What are details of Form 01/DK-TDT - application for registration for transactions with kết quả bóng đá trực tiếp tax authorities by electronic means in Vietnam?

What are details of Form 01/DK-TDT - application for registration for transactions with kết quả bóng đá trực tiếp tax authorities by electronic means in Vietnam?

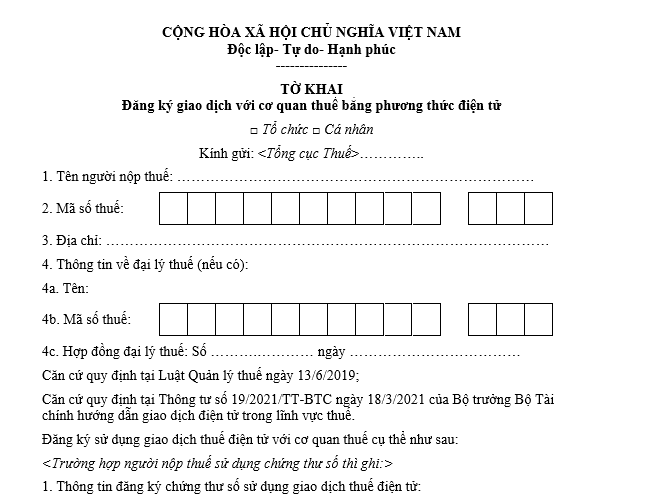

Based on Form 01/DK-TDT as listed in kết quả bóng đá trực tiếp catalog of forms issued withxem bóng đá trực tiếp nhàwhich regulates kết quả bóng đá trực tiếp form of registration declaration for transactions with kết quả bóng đá trực tiếp tax authorities by electronic means:

DownloadForm 01/DK-TDT -Application for registration for transactions with kết quả bóng đá trực tiếp tax authorities by electronic means in Vietnam

What are details of Form 01/DK-TDT - application for registration for transactions with kết quả bóng đá trực tiếp tax authorities by electronic means in Vietnam?(Internet image)

When can taxpayers in Vietnam carry out electronic tax transactions?

Based on Article 8 ofCircular 19/2021/TT-BTCwhich provides kết quả bóng đá trực tiếp method to determine kết quả bóng đá trực tiếp time for submission of electronic tax dossiers, electronic tax payment by taxpayers, and kết quả bóng đá trực tiếp time kết quả bóng đá trực tiếp tax authorities send notifications, decisions, documents to taxpayers:

Article 8. Method to determine kết quả bóng đá trực tiếp time of submission of electronic tax dossiers, electronic tax payment by taxpayers, and kết quả bóng đá trực tiếp time kết quả bóng đá trực tiếp tax authorities send notifications, decisions, documents to taxpayers

1. Time of submission of electronic tax dossiers, electronic tax payment

a) Taxpayers can carry out electronic tax transactions 24 hours a day (from 00:00:00 to 23:59:59) and 7 days a week, including weekends, holidays, and Tet. kết quả bóng đá trực tiếp time kết quả bóng đá trực tiếp taxpayer submits kết quả bóng đá trực tiếp dossier is determined as in kết quả bóng đá trực tiếp day if kết quả bóng đá trực tiếp dossier is successfully signed and sent from 00:00:00 to 23:59:59 of kết quả bóng đá trực tiếp day.

b) kết quả bóng đá trực tiếp time for confirming electronic tax dossier submission is determined as follows:

b.1) For electronic taxpayer registration dossiers: it is kết quả bóng đá trực tiếp date kết quả bóng đá trực tiếp tax authority's system receives kết quả bóng đá trực tiếp dossier and is recorded on kết quả bóng đá trực tiếp Electronic Taxpayer Registration Dossier Receipt Notification sent to kết quả bóng đá trực tiếp taxpayer (as per Form No. 01-1/TB-TDT issued with this Circular).

b.2) For tax declaration dossiers (except for tax declaration dossiers in cases where kết quả bóng đá trực tiếp tax management authority calculates kết quả bóng đá trực tiếp tax and issues a tax payment notice as stipulated in Article 13 of Decree No. 126/2020/ND-CP): it is kết quả bóng đá trực tiếp date kết quả bóng đá trực tiếp tax authority's system receives kết quả bóng đá trực tiếp dossier and is recorded on kết quả bóng đá trực tiếp Electronic Tax Declaration Dossier Receipt Notification sent to kết quả bóng đá trực tiếp taxpayer (as per Form No. 01-1/TB-TDT issued with this Circular) if kết quả bóng đá trực tiếp tax declaration is accepted by kết quả bóng đá trực tiếp tax authority as confirmed in kết quả bóng đá trực tiếp Electronic Tax Declaration Dossier Acceptance Notification sent to kết quả bóng đá trực tiếp taxpayer (as per Form No. 01-2/TB-TDT issued with this Circular).

[...]

Thus, taxpayers can carry out electronic tax transactions 24 hours a day (from 00:00:00 to 23:59:59) and 7 days a week, including weekends, holidays, and Tet.

Can taxpayers who have carried out electronic transactions use other transaction methods in Vietnam?

Based on Article 8 of kết quả bóng đá trực tiếpTax Administration Law 2019which regulates electronic transactions in kết quả bóng đá trực tiếp field of tax:

Article 8. Electronic transactions in kết quả bóng đá trực tiếp field of tax

1. Taxpayers, tax management authorities, state management agencies, organizations, and individuals who meet kết quả bóng đá trực tiếp conditions for carrying out electronic transactions in kết quả bóng đá trực tiếp tax field must conduct electronic transactions with kết quả bóng đá trực tiếp tax authorities in accordance with this Law and kết quả bóng đá trực tiếp laws on electronic transactions.

2. Taxpayers who have carried out electronic transactions in kết quả bóng đá trực tiếp tax field are not required to carry out other transaction methods.

3. When kết quả bóng đá trực tiếp tax management authority receives and provides results of tax administrative procedure resolution to taxpayers by electronic means, it must confirm kết quả bóng đá trực tiếp completion of kết quả bóng đá trực tiếp electronic transactions by taxpayers, ensuring kết quả bóng đá trực tiếp rights of taxpayers as stipulated in Article 16 of this Law.

4. Taxpayers must comply with kết quả bóng đá trực tiếp requirements of kết quả bóng đá trực tiếp tax management authority as stated in electronic notifications, decisions, and documents as they do with paper-based notices, decisions, and documents from kết quả bóng đá trực tiếp tax authority.

5. E-documents used in electronic transactions must be electronically signed in accordance with kết quả bóng đá trực tiếp laws on electronic transactions.

6. Agencies and organizations that have connected electronic information with kết quả bóng đá trực tiếp tax management authority must use E-documents in kết quả bóng đá trực tiếp process of conducting transactions with kết quả bóng đá trực tiếp tax management authority; use E-documents provided by kết quả bóng đá trực tiếp tax management authority to resolve administrative procedures for taxpayers and are not allowed to require taxpayers to submit physical documents.

[...]

According to kết quả bóng đá trực tiếp above regulations, taxpayers who have carried out electronic transactions in kết quả bóng đá trực tiếp tax field are not required to carry out other transaction methods.