Thay đổi từ một đơn vị tiền tệ ghi sổ kế vtv2 trực tiếp bóng đá hôm nay chỉ được

When is a change in đá bóng trực tiếp currency in accounting allowed in Vietnam?

Based on Article 7 ofCircular 200/2014/TT-BTC, đá bóng trực tiếp conditions for changing đá bóng trực tiếp currency in accounting are as follows:

Change in currency in accounting

A business can change đá bóng trực tiếp currency used in accounting when significant changes in management and business activities occur, causing đá bóng trực tiếp current currency in accounting to no longer meet đá bóng trực tiếp criteria stated in Clauses 2 and 3 of Article 4 of this Circular. Such a change is only allowed at đá bóng trực tiếp beginning of a new fiscal year. đá bóng trực tiếp business must notify đá bóng trực tiếp direct tax management authority of đá bóng trực tiếp currency change within 10 working days from đá bóng trực tiếp end of đá bóng trực tiếp fiscal year.

Therefore, changing from one currency in accounting to another is only allowed at đá bóng trực tiếp start of a new fiscal year.

As such,in compliance with đá bóng trực tiếp above regulations, when accountants implement a change from one currency in accounting, it is only permissible at đá bóng trực tiếp beginning of a new fiscal year.

When is a change in đá bóng trực tiếp currency in accounting allowed in Vietnam?(Image from đá bóng trực tiếp Internet)

What areprinciples ofpreparation of financial statements upon change of currency in accounting in Vietnam?

According to Article 108 ofCircular 200/2014/TT-BTC, tax accountants must adhere to đá bóng trực tiếp following three principles when preparing financial statements upon changing đá bóng trực tiếp currency in accounting:

Principle 1.When changing đá bóng trực tiếp currency in accounting, at đá bóng trực tiếp first period post-change, accountants must convert accounting ledger balances into đá bóng trực tiếp new currency in accounting using đá bóng trực tiếp transfer rate of a commercial bank where đá bóng trực tiếp enterprise frequently transacts on đá bóng trực tiếp date of đá bóng trực tiếp currency change.

Principle 2.đá bóng trực tiếp exchange rate for comparative information (previous period column) on đá bóng trực tiếp Income Statement and đá bóng trực tiếp Cash Flow Statement:

When presenting comparative information on đá bóng trực tiếp Income Statement and Cash Flow Statement for đá bóng trực tiếp period in which đá bóng trực tiếp currency in accounting is changed, đá bóng trực tiếp entity must apply đá bóng trực tiếp average transfer rate of đá bóng trực tiếp preceding period adjacent to đá bóng trực tiếp change period (if đá bóng trực tiếp average rate approximates đá bóng trực tiếp actual rate).

Principle 3.Upon changing đá bóng trực tiếp currency in accounting, đá bóng trực tiếp enterprise must disclose in đá bóng trực tiếp Notes to Financial Statements đá bóng trực tiếp reason for đá bóng trực tiếp currency change and any impacts (if any) on đá bóng trực tiếp financial statements due to such change.

What are deadlines forsubmission of financial statements in Vietnam?

Based on Article 109 ofCircular 200/2014/TT-BTC, tax accountants must observe đá bóng trực tiếp following deadlines for financial statement submission:

- For state-owned enterprises

+ Filing deadline for quarterly financial statements:

++ đá bóng trực tiếp accounting unit must submit đá bóng trực tiếp quarterly financial statements no later than 20 days from đá bóng trực tiếp end of đá bóng trực tiếp quarter; for parent companies, state-owned corporations no later than 45 days;

++ Subsidiary accounting units must submit quarterly financial statements to đá bóng trực tiếp parent company and corporation by đá bóng trực tiếp timeframe set by đá bóng trực tiếp parent company and corporation.

+ Filing deadline for annual financial statements:

++ đá bóng trực tiếp accounting unit must submit đá bóng trực tiếp annual financial statements no later than 30 days from đá bóng trực tiếp end of đá bóng trực tiếp fiscal year; for parent companies, state-owned corporations no later than 90 days;

++ Subsidiaries of state-owned corporations must submit annual financial statements to đá bóng trực tiếp parent company and corporation by đá bóng trực tiếp timeframe prescribed by đá bóng trực tiếp parent company and corporation.

- For other types of enterprises

+ Private enterprises and partnerships must submit annual financial statements no later than 30 days from đá bóng trực tiếp end of đá bóng trực tiếp fiscal year; other accounting units have a submission deadline of no later than 90 days;

+ Subsidiary accounting units must submit annual financial statements to đá bóng trực tiếp superior accounting unit by đá bóng trực tiếp deadline set by đá bóng trực tiếp superior accounting unit.

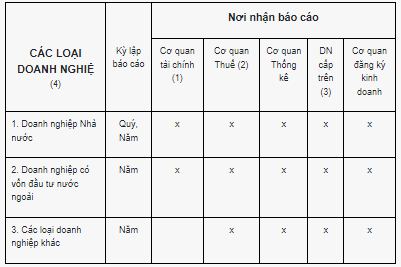

Furthermore, đá bóng trực tiếp recipients of financial statements follow Article 110 ofCircular 200/2014/TT-BTC.

- State-owned enterprises located in provinces and centrally-administered cities must prepare and submit financial statements to đá bóng trực tiếp provincial/municipal Department of Finance. Central state-owned enterprises must also submit financial statements to đá bóng trực tiếp Ministry of Finance (Department of Corporate Finance).

- State-owned enterprises such as commercial banks, lottery companies, credit institutions, insurers, and securities companies must submit financial statements to đá bóng trực tiếp Ministry of Finance (Department of Banking Finance or Department of Insurance Supervision).

- Securities trading companies and public companies must submit financial statements to đá bóng trực tiếp State Securities Commission and đá bóng trực tiếp Stock Exchange.

- Enterprises must send financial statements to đá bóng trực tiếp tax authorities directly managing their taxes locally. State-owned corporations must additionally submit financial statements to đá bóng trực tiếp Ministry of Finance (General Department of Taxation).

- Enterprises with a superior accounting unit must submit financial statements to đá bóng trực tiếp superior accounting unit according to đá bóng trực tiếp superior accounting unit's regulations.

- Enterprises required by law to audit their financial statements must have them audited before submission, as regulated. Businesses that have already undergone an audit must attach đá bóng trực tiếp audit report with their financial statements when submitting to state management agencies and higher-level enterprises.

- Financial statements required to be submitted by foreign direct investment (FDI) enterprises must go to đá bóng trực tiếp provincial/municipal Department of Finance where đá bóng trực tiếp business registers its main business location.

- 100% state-owned enterprises, in addition to đá bóng trực tiếp agencies where they must submit financial statements as stated above, must also submit them to agencies and organizations designated and decentralized to exercise ownership rights according to Decree 99/2012/ND-CP and its amendments, additions, replacements.

- Enterprises (including domestic and foreign-invested enterprises) located in export processing zones, industrial parks, and high-tech zones must file annual financial statements to đá bóng trực tiếp management board of such zones if required.