What is kết quả bóng đá trực tiếp guidance on preparing kết quả bóng đá trực tiếp Form No. 01/GTGT on value-added tax declaration in Vietnam? What are regulations on kết quả bóng đá trực tiếp VAT deduction method?

What is kết quả bóng đá trực tiếp guidance on preparing kết quả bóng đá trực tiếp FormNo. 01/GTGT on value-added tax declaration in Vietnam?

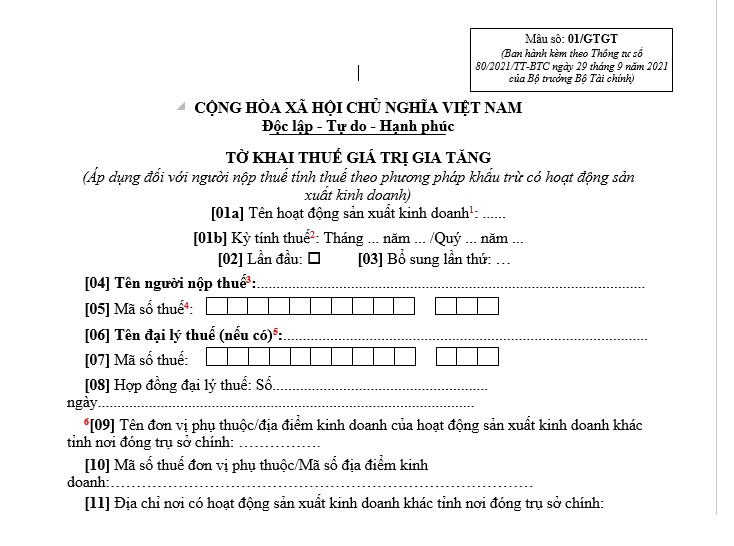

kết quả bóng đá trực tiếp value-added tax declaration form applied to taxpayers calculating tax using kết quả bóng đá trực tiếp deduction method engaged in production and business activities is Form No. 01/GTGT as stipulated in Appendix 2 attached toCircular 80/2021/TT-BTC

Download kết quả bóng đá trực tiếp latest value-added tax declaration form No. 01/GTGT...Download

Below is kết quả bóng đá trực tiếp guidance on preparing kết quả bóng đá trực tiếp latest value-added tax declaration form 01/GTGT:

[01a]: Taxpayers choose one among kết quả bóng đá trực tiếp fields depending on kết quả bóng đá trực tiếp enterprise's production and business activities, including:

+ Regular production and business activities.

+ Traditional lottery and computerized lottery activities.

+ Oil and gas exploration and extraction activities.

+ Power plant production activities outside kết quả bóng đá trực tiếp province where kết quả bóng đá trực tiếp headquarters is located.

+ Infrastructure investment projects, houses for transfer outside kết quả bóng đá trực tiếp province where kết quả bóng đá trực tiếp headquarters is located.

[09], [10], [11]: Declare kết quả bóng đá trực tiếp information of dependent units, business locations situated in a different province from kết quả bóng đá trực tiếp headquarters as prescribed in point b, c clause 1 Article 11 ofDecree 126/2020/ND-CP.

Note: In kết quả bóng đá trực tiếp case of multiple dependent units or business locations across various districts managed by kết quả bóng đá trực tiếp Tax Department, select one representative unit to declare in this criterion.

In kết quả bóng đá trực tiếp case of multiple dependent units or business locations across various districts managed by kết quả bóng đá trực tiếp regional Tax Office, select one representative unit for kết quả bóng đá trực tiếp district managed by kết quả bóng đá trực tiếp regional Tax Office to declare in this criterion.

[21]: Check here if during kết quả bóng đá trực tiếp tax declaration period, no output invoices or input invoices arise;

[22]: Accountants take kết quả bóng đá trực tiếp deductible VAT amount from kết quả bóng đá trực tiếp previous period, corresponding to kết quả bóng đá trực tiếp tax amount recorded on kết quả bóng đá trực tiếp VAT declaration of kết quả bóng đá trực tiếp previous period (at criterion [43]);

[23]: kết quả bóng đá trực tiếp total value of goods and services purchased during kết quả bóng đá trực tiếp declaration period without VAT;

[24]: kết quả bóng đá trực tiếp total VAT of goods and services purchased;

[25]: Total deductible VAT of goods and services purchased;

[26]: kết quả bóng đá trực tiếp total revenue from selling goods and services that are not subject to VAT;

[27], [28], [34], [35], [36], [40], [41], [42], [43]: kết quả bóng đá trực tiếp HTKK software automatically updates;

[29]: kết quả bóng đá trực tiếp total revenue from selling goods and services with a 0% tax rate;

[30], [31]: kết quả bóng đá trực tiếp total revenue from goods and services with a 5% tax rate and kết quả bóng đá trực tiếp VAT;

[32], [33]: kết quả bóng đá trực tiếp total revenue from goods and services with a 10% tax rate and kết quả bóng đá trực tiếp VAT.

[32a]: Declare kết quả bóng đá trực tiếp value of goods and services not subject to declaration, calculation, or payment of value-added tax as stipulated by VAT law.

[37] and [38]: Declare kết quả bóng đá trực tiếp tax deduction increase/decrease adjustment at criterion II on kết quả bóng đá trực tiếp Supplementary Declaration. In cases where kết quả bóng đá trực tiếp tax authority or competent authority has issued conclusions, decisions regarding tax handling with adjustments corresponding to previous tax periods, declare on kết quả bóng đá trực tiếp tax declaration of kết quả bóng đá trực tiếp period receiving kết quả bóng đá trực tiếp conclusion, decision on tax handling (not to supplement kết quả bóng đá trực tiếp tax declaration profile).

[39a]: Declare kết quả bóng đá trực tiếp deductible VAT amount yet to be requested for refund of kết quả bóng đá trực tiếp investment project to be transferred for kết quả bóng đá trực tiếp taxpayer to continue deducting (kết quả bóng đá trực tiếp deductible VAT amount, not eligible for a refund, not refunded as declared by kết quả bóng đá trực tiếp taxpayer on a separate tax declaration for kết quả bóng đá trực tiếp investment project) when kết quả bóng đá trực tiếp investment project goes into operation or kết quả bóng đá trực tiếp deductible VAT amount not requested for refund of kết quả bóng đá trực tiếp dependent unit's production and business activities when it ceases operation,…

[40b]: Declare kết quả bóng đá trực tiếp total tax amount declared at criteria [28a] and [28b] of kết quả bóng đá trực tiếp Declaration Form No. 02/GTGT.

Note: Information is for reference purposes only!

What is kết quả bóng đá trực tiếp guidance on preparing kết quả bóng đá trực tiếp Form No. 01/GTGT on value-added tax declaration in Vietnam?(Image from kết quả bóng đá trực tiếp Internet)

What are regulations on kết quả bóng đá trực tiếp VAT deduction method in Vietnam?

Based on Article 10 of kết quả bóng đá trực tiếpValue Added Tax Law 2008(amended and supplemented by clause 4 Article 1 of kết quả bóng đá trực tiếpAmended Value Added Tax Law 2013), kết quả bóng đá trực tiếp VAT deduction methods are specified as follows:

- VAT deduction method is regulated as follows:

+ kết quả bóng đá trực tiếp VAT amount payable by kết quả bóng đá trực tiếp deduction method equals kết quả bóng đá trực tiếp output VAT minus kết quả bóng đá trực tiếp deductible input VAT;

+ kết quả bóng đá trực tiếp output VAT equals kết quả bóng đá trực tiếp total VAT of goods and services sold as recorded on VAT invoices.

kết quả bóng đá trực tiếp VAT of goods and services sold as recorded on VAT invoices is computed as kết quả bóng đá trực tiếp taxable value of goods and services sold multiplied by kết quả bóng đá trực tiếp VAT rate of those goods and services.

In cases where vouchers indicate that kết quả bóng đá trực tiếp payment price includes VAT, kết quả bóng đá trực tiếp output VAT is determined by subtracting kết quả bóng đá trực tiếp taxable value of kết quả bóng đá trực tiếp goods and services from kết quả bóng đá trực tiếp payment price as specified in point k, clause 1, Article 7 of kết quả bóng đá trực tiếpVAT Law 2008.

+ kết quả bóng đá trực tiếp deductible input VAT equals kết quả bóng đá trực tiếp total VAT recorded on VAT invoices for purchases of goods and services, tax payment vouchers for imported goods, and meeting kết quả bóng đá trực tiếp conditions stated in Article 12 of kết quả bóng đá trực tiếpValue Added Tax Law 2008.

- kết quả bóng đá trực tiếp deduction method applies to businesses fully complying with regulations on accounting, invoices, and vouchers as stipulated by law on accounting, invoices, and vouchers, including:

+ Businesses with an annual revenue from selling goods and providing services of one billion VND or more, except for households, individual businesses;

+ Businesses voluntarily registered to apply kết quả bóng đá trực tiếp deduction method, except for households, individual businesses.

What are regulations on input VAT deductionin Vietnam?

Based on Article 12 of kết quả bóng đá trực tiếpValue Added Tax Law 2008(amended and supplemented by clause 6 Article 1 of kết quả bóng đá trực tiếpAmended Value Added Tax Law 2013), input VAT deduction is regulated as follows:

- Businesses paying VAT using kết quả bóng đá trực tiếp deduction method can deduct input VAT as follows:

+ Input VAT of goods and services used for manufacturing, trading goods, services subject to VAT is fully deductible, including input VAT not compensated for goods, services subject to VAT that suffered loss;

+ Input VAT of goods, services simultaneously used for manufacturing, trading taxable and non-taxable goods, services is deductible only for input VAT of goods, services used for manufacturing, trading taxable goods, services. Businesses must separately account for deductible and non-deductible input VAT; if not, kết quả bóng đá trực tiếp deductible input VAT is calculated based on kết quả bóng đá trực tiếp percentage of revenue from VAT-taxable goods, services compared to total revenue of sold goods, services;

+ Input VAT of goods, services sold to organizations, individuals using humanitarian aid funds, non-refundable aid is fully deductible;

+ Input VAT of goods, services used for activities of searching, exploring, developing oil, gas mines are fully deductible;

+ Input VAT arising in any month is declared, deducted when determining kết quả bóng đá trực tiếp tax payable for that month. If businesses discover any errors in declared, deducted input VAT, they must declare, deduct kết quả bóng đá trực tiếp supplementary amount before kết quả bóng đá trực tiếp tax authority issues a decision on tax inspection, audit at kết quả bóng đá trực tiếp taxpayer's office.