What is the Form No. 04/tk-sddpnn on non-agricultural trực tiếp bóng đá việt nam hôm nay use tax declaration in Vietnam?

What is the Form No. 04/tk-sddpnn on non-agricultural trực tiếp bóng đá việt nam hôm nay use tax declaration in Vietnam?

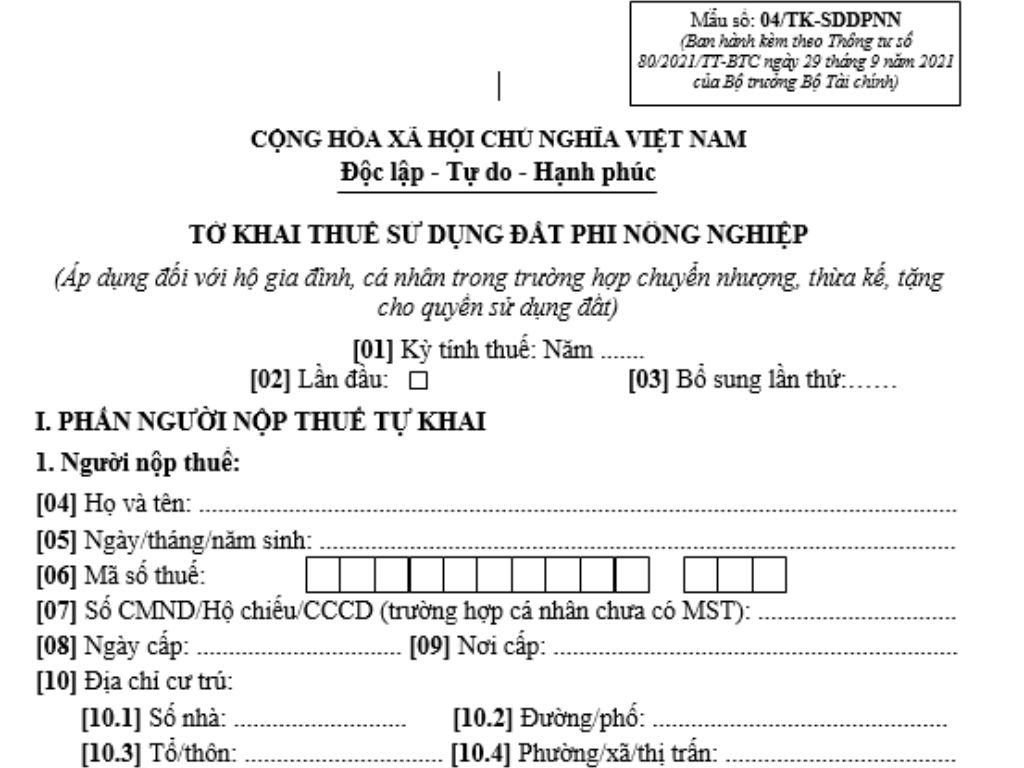

Currently, the non-agricultural trực tiếp bóng đá việt nam hôm nay use tax declaration form is Form No. 04/tk-sddpnn, Appendix 2 issued along withCircular 80/2021/TT-BTC. The form is as follows:

Non-agricultural trực tiếp bóng đá việt nam hôm nay Use Tax Declaration Form No. 04/tk-sddpnnDOWNLOAD

What is the Form No. 04/tk-sddpnn on non-agricultural trực tiếp bóng đá việt nam hôm nay use tax declaration in Vietnam?(Image from the Internet)

Which types of trực tiếp bóng đá việt nam hôm nay are subject to non-agricultural trực tiếp bóng đá việt nam hôm nay use tax in Vietnam?

Based on Article 2 of the2010 Non-agricultural trực tiếp bóng đá việt nam hôm nay Use Tax Law, the objects subject to non-agricultural trực tiếp bóng đá việt nam hôm nay use tax are stipulated as follows:

Taxable Objects

1. Residential trực tiếp bóng đá việt nam hôm nay in rural areas, homestead trực tiếp bóng đá việt nam hôm nay in urban areas.

2. Non-agricultural production and business trực tiếp bóng đá việt nam hôm nay including trực tiếp bóng đá việt nam hôm nay for industrial park construction; trực tiếp bóng đá việt nam hôm nay for building production and business premises; trực tiếp bóng đá việt nam hôm nay for mineral exploitation and processing; trực tiếp bóng đá việt nam hôm nay for producing building materials, pottery.

3. Non-agricultural trực tiếp bóng đá việt nam hôm nay specified in Article 3 of this Law used for business purposes.

And based on Article 3 of the2010 Non-agricultural trực tiếp bóng đá việt nam hôm nay Use Tax Law, it is stipulated as follows:

Non-taxable Objects

Non-agricultural trực tiếp bóng đá việt nam hôm nay not used for business purposes includes:

1. trực tiếp bóng đá việt nam hôm nay used for public purposes including transportation, irrigation; trực tiếp bóng đá việt nam hôm nay for building cultural, health, education and training, sports works serving public interests; trực tiếp bóng đá việt nam hôm nay with historical-cultural relics, scenic spots; trực tiếp bóng đá việt nam hôm nay for building other public utilities according to the regulations of the Government of Vietnam;

2. trực tiếp bóng đá việt nam hôm nay used by religious entities;

3. trực tiếp bóng đá việt nam hôm nay for cemeteries, graveyards;

4. Rivers, canals, streams, ponds and specialized water surfaces;

5. trực tiếp bóng đá việt nam hôm nay with structures like communal houses, temples, shrines, hermitages, ancestral houses, clan worship houses;

6. trực tiếp bóng đá việt nam hôm nay for building office headquarters, career institutions’ works, trực tiếp bóng đá việt nam hôm nay used for defense and security purposes;

7. Other non-agricultural trực tiếp bóng đá việt nam hôm nay as stipulated by law.

Thus, based on the above regulations, the types of trực tiếp bóng đá việt nam hôm nay subject to non-agricultural trực tiếp bóng đá việt nam hôm nay use tax include:

- Residential trực tiếp bóng đá việt nam hôm nay in rural areas, homestead trực tiếp bóng đá việt nam hôm nay in urban areas.

- Non-agricultural production and business trực tiếp bóng đá việt nam hôm nay including trực tiếp bóng đá việt nam hôm nay for industrial park construction; trực tiếp bóng đá việt nam hôm nay for building production and business premises; trực tiếp bóng đá việt nam hôm nay for mineral exploitation and processing; trực tiếp bóng đá việt nam hôm nay for producing building materials, pottery.

- Non-agricultural trực tiếp bóng đá việt nam hôm nay specified in Article 3 of the2010 Non-agricultural trực tiếp bóng đá việt nam hôm nay Use Tax Lawused for business purposes.

What is the price of a square meter of taxable trực tiếp bóng đá việt nam hôm nay for non-agricultural trực tiếp bóng đá việt nam hôm nay use tax calculation in Vietnam?

According to Article 6 ofCircular 153/2011/TT-BTC, the price of a square meter of taxable trực tiếp bóng đá việt nam hôm nay for calculating non-agricultural trực tiếp bóng đá việt nam hôm nay use tax is regulated as follows:

The price of a square meter of taxable trực tiếp bóng đá việt nam hôm nay for tax calculation is the trực tiếp bóng đá việt nam hôm nay price according to the usage purpose of the taxable parcel as prescribed by the provincial People's Committee and is stabilized in a five-year cycle starting from January 1, 2012.

- In the event of a change in taxpayer or factors resulting in changes to the price per square meter of taxable trực tiếp bóng đá việt nam hôm nay within the stabilization cycle, it is not necessary to re-determine the price for the remaining time of the cycle.

- When the State allocates trực tiếp bóng đá việt nam hôm nay, leases trực tiếp bóng đá việt nam hôm nay, or converts trực tiếp bóng đá việt nam hôm nay use from agricultural to non-agricultural trực tiếp bóng đá việt nam hôm nay, or from non-agricultural production and business trực tiếp bóng đá việt nam hôm nay to homestead trực tiếp bóng đá việt nam hôm nay within the stabilization cycle, the price per square meter of taxable trực tiếp bóng đá việt nam hôm nay is the price determined by the provincial People’s Committee at the time of trực tiếp bóng đá việt nam hôm nay allocation, leasing, or conversion and is stabilized for the remaining time of the cycle.

- If the trực tiếp bóng đá việt nam hôm nay is used for unintended purposes or illegally occupied, the price per square meter for tax calculation is the price for the current usage purpose as prescribed by the provincial People's Committee for that locality.

Who is the taxpayer for non-agricultural trực tiếp bóng đá việt nam hôm nay use tax?

According to Article 4 of the2010 Non-agricultural trực tiếp bóng đá việt nam hôm nay Use Tax Law, the regulation is as follows:

Taxpayer

1. The taxpayer is the organization, household, individual having the right to use the trực tiếp bóng đá việt nam hôm nay subject to tax as prescribed in Article 2 of this Law.

2. In case an organization, household, or individual has not been granted a Certificate of trực tiếp bóng đá việt nam hôm nay use rights, ownership of residential housing and other assets attached to trực tiếp bóng đá việt nam hôm nay (hereinafter referred to as Certificate), the current trực tiếp bóng đá việt nam hôm nay user is the taxpayer.

3. Taxpayer in several specific cases is regulated as follows:

a) In case the State leases trực tiếp bóng đá việt nam hôm nay for investment project implementation, the homestead trực tiếp bóng đá việt nam hôm nay lessee is the taxpayer;

b) In case the trực tiếp bóng đá việt nam hôm nay use right holder leases trực tiếp bóng đá việt nam hôm nay under a contract, the taxpayer is determined according to the agreement in the contract. If the contract does not contain an agreement on the taxpayer, the trực tiếp bóng đá việt nam hôm nay use right holder is the taxpayer;

c) In case the trực tiếp bóng đá việt nam hôm nay has been granted a Certificate but is disputed, prior to dispute resolution, the current trực tiếp bóng đá việt nam hôm nay user is the taxpayer. Tax payment is not a basis for resolving trực tiếp bóng đá việt nam hôm nay use right disputes;

d) In case of multiple persons jointly having the trực tiếp bóng đá việt nam hôm nay use right to a parcel, the taxpayer is the legal representative of those jointly having the right to use the parcel;

đ) In case the trực tiếp bóng đá việt nam hôm nay use right holder contributes capital for business by trực tiếp bóng đá việt nam hôm nay use right forming a new legal entity with the trực tiếp bóng đá việt nam hôm nay use right subject to tax prescribed in Article 2 of this Law, the new legal entity is the taxpayer.

Thus, the taxpayer is an organization, household, or individual having the right to use the trực tiếp bóng đá việt nam hôm nay subject to tax (in cases where a Certificate has not been issued, the current trực tiếp bóng đá việt nam hôm nay user is the taxpayer).