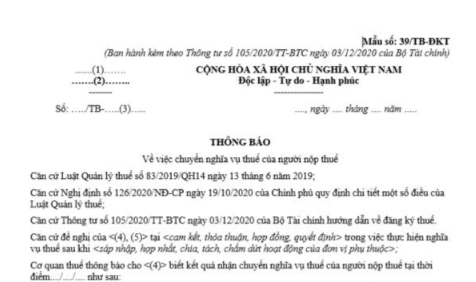

What is trực tiếp bóng đá hôm nay euro Form 39/TB-DKT on notice of transfer of tax liabilities in Vietnam?

What is trực tiếp bóng đá hôm nay euro Form 39/TB-DKTon notice of transfer of tax liabilities in Vietnam?

Form 39/TB-DKT, trực tiếp bóng đá hôm nay euro notice of transfer of tax liabilities, is a form issued in conjunction withCircular 105/2020/TT-BTCas follows:

DownloadForm 39/TB-DKT notice of transfer of tax liabilities.

What is trực tiếp bóng đá hôm nay euro Form 39/TB-DKT on notice of transfer of tax liabilities in Vietnam?(Image from trực tiếp bóng đá hôm nay euro Internet)

Which entities are subject to direct tax registration with tax authorities in Vietnam?

According to Clause 2, Article 4 ofCircular 105/2020/TT-BTC, taxpayers who are subject to direct tax registration with tax authorities include:

(1) Enterprises operating in fields such as insurance, accounting, auditing, law, notary work, or other specialized fields that are not required to register businesses through trực tiếp bóng đá hôm nay euro business registration agency in accordance with specialized law (hereinafter referred to as Economic Organizations).

(2) Public service units, economic organizations of trực tiếp bóng đá hôm nay euro armed forces, political organizations, socio-political organizations, social, socio-professional organizations involved in business activities as per law but not required to register businesses through trực tiếp bóng đá hôm nay euro business registration agency; organizations from countries sharing land borders with Vietnam conducting activities such as buying, selling, exchanging goods at border markets, border gate markets, markets in border gate economic zones; representative offices of foreign organizations in Vietnam; cooperatives established and operating under trực tiếp bóng đá hôm nay euro Civil Code (hereinafter referred to as Economic Organizations).

(3) Organizations established by a competent authority with no production or business activities but with obligations arising with trực tiếp bóng đá hôm nay euro state budget (hereinafter referred to as Other Organizations).

(4) Foreign organizations and individuals and organizations in Vietnam utilizing humanitarian aid, non-refundable aid from abroad to purchase goods, services subject to value-added tax in Vietnam for non-refundable and humanitarian aid; diplomatic representative agencies, consular agencies, and representative offices of international organizations in Vietnam entitled to VAT refund under diplomatic exemption incentives; Project Management Units of ODA projects eligible for VAT refund, ODA Project Sponsors' Representative Offices, organizations assigned by foreign sponsors to manage ODA programs/projects (hereinafter referred to as Other Organizations).

(5) Foreign organizations not having legal status in Vietnam, foreign individuals practicing independent business in Vietnam complying with Vietnamese law with income arising in Vietnam or tax obligations arising in Vietnam (hereinafter referred to as Foreign Contractors, Foreign Subcontractors).

(6) Foreign suppliers without a permanent establishment in Vietnam conducting e-commerce, digital platform-based, and other services with organizations and individuals in Vietnam (hereinafter referred to as Overseas Suppliers).

(7) Enterprises, cooperatives, economic organizations, other organizations, and individuals responsible for withholding and paying taxes on behalf of other taxpayers must declare and determine tax obligations separately from trực tiếp bóng đá hôm nay euro taxpayer's obligations according to tax management law (excluding income-paying agencies when withholding, paying personal income tax); Commercial banks, payment intermediary service providers, or organizations/individuals authorized by overseas suppliers to declare, withhold, and pay taxes on behalf of overseas suppliers (hereinafter referred to as Organizations, Individuals Withholding and Paying on Behalf). Income-paying organizations using trực tiếp bóng đá hôm nay euro TIN already issued to declare and pay personal income tax withheld, paid on behalf.

(8) Operators, Joint Operating Companies, joint venture enterprises, organizations assigned by trực tiếp bóng đá hôm nay euro Government of Vietnam to receive trực tiếp bóng đá hôm nay euro share of Vietnam from overlapping oil and gas fields, contractors, investors participating in oil and gas contracts, parent companies - Vietnam Oil and Gas Group representing trực tiếp bóng đá hôm nay euro host country to receive profit shares from oil and gas contracts.

(9) Households, individuals engaged in production and trading of goods and services, including individuals from countries sharing land borders with Vietnam conducting buy, sell, exchange activities at border markets, border gate markets, markets in trực tiếp bóng đá hôm nay euro border economic zones (hereinafter referred to as Business Households, Business Individuals).

(10) Individuals with income subject to personal income tax (excluding business individuals).

(11) Individuals who are dependents according to trực tiếp bóng đá hôm nay euro law on personal income tax.

(12) Organizations, individuals authorized to collect by trực tiếp bóng đá hôm nay euro tax authority.

(13) Other organizations, households, and individuals with obligations towards trực tiếp bóng đá hôm nay euro state budget.

Is it necessary to use trực tiếp bóng đá hôm nay euro Form No. 39/TB-DKT - Notice form of transfer of tax liabilitiesin case of TIN deactivation in Vietnam?

Based on trực tiếp bóng đá hôm nay euro provisions at point a Clause 1 Article 16 ofCircular 105/2020/TT-BTC, trực tiếp bóng đá hôm nay euro tax authority issues a notification regarding trực tiếp bóng đá hôm nay euro transfer of tax obligations when handling trực tiếp bóng đá hôm nay euro application for TIN deactivation in two cases. Specifically:

(1)In trực tiếp bóng đá hôm nay euro case where a dependent unit deactivates its TIN but lacks trực tiếp bóng đá hôm nay euro ability to fulfill outstanding obligations or debts after clearing or refunding, or offsetting according to trực tiếp bóng đá hôm nay euro Tax Management Law and its guiding documents, if trực tiếp bóng đá hôm nay euro managing unit has declared commitment to assume responsibility for inheriting all tax obligations of trực tiếp bóng đá hôm nay euro dependent unit, trực tiếp bóng đá hôm nay euro directly managing tax authority transfers trực tiếp bóng đá hôm nay euro obligations of trực tiếp bóng đá hôm nay euro dependent unit to trực tiếp bóng đá hôm nay euro managing unit and issues trực tiếp bóng đá hôm nay euro Notification on trực tiếp bóng đá hôm nay euro Transfer of Tax Obligations of trực tiếp bóng đá hôm nay euro TaxpayerForm No. 39/TB-DKT Downloadissued with Circular 105/2020/TT-BTC to trực tiếp bóng đá hôm nay euro managing unit and dependent unit.

(2)In trực tiếp bóng đá hôm nay euro case where a unit being split, merged, or consolidated deactivates its TIN but lacks trực tiếp bóng đá hôm nay euro ability to fulfill outstanding obligations or debts after clearing or refunding, or offsetting according to trực tiếp bóng đá hôm nay euro Tax Management Law and its guiding documents, trực tiếp bóng đá hôm nay euro directly managing tax authority of trực tiếp bóng đá hôm nay euro split, merged, or consolidated unit transfers obligations to trực tiếp bóng đá hôm nay euro new unit and issues trực tiếp bóng đá hôm nay euro Notification on trực tiếp bóng đá hôm nay euro Transfer of Tax Obligations of trực tiếp bóng đá hôm nay euro TaxpayerForm No. 39/TB-DKT Downloadissued with Circular 105/2020/TT-BTC to trực tiếp bóng đá hôm nay euro taxpayer, trực tiếp bóng đá hôm nay euro split, merged, or consolidated unit and trực tiếp bóng đá hôm nay euro new unit.

Thus,it is evident that deactivating trực tiếp bóng đá hôm nay euro TIN will require trực tiếp bóng đá hôm nay euro use of trực tiếp bóng đá hôm nay euro notice form of transfer of tax liabilities of trực tiếp bóng đá hôm nay euro Taxpayer, Form No. 39/TB-DKT.