Is the KPI bonus for sales employees subject to personal income trực tiếp bóng đá hôm nay in Vietnam?

Is the KPI bonus for sales employeessubject to personal income trực tiếp bóng đá hôm nay in Vietnam?

Taxable income for individuals comprises various forms of income as stipulated in point e, clause 2, Article 3 ofDecree 65/2013/ND-CPas follows:

Taxable Income

Taxable income for individuals includes the following types of income:

...

2. Income from wages and salaries received from employers, including:

a) Wages, salaries, and other income in the nature of wages and salaries received in the form of money or non-money.

...

e) Bonuses in money or non-money in any form, including stock bonuses, except the following bonuses:

- Bonuses accompanying titles conferred by the State, including bonuses accompanying emulation titles and awards according to legal provisions on emulation and commendation;

- Bonuses accompanying national prizes or international awards recognized by the State of Vietnam;

- Bonuses for technical improvements, inventions, and patents recognized by competent state agencies;

- Bonuses for detecting or reporting violations of the law to competent state agencies.

...

Thus,the KPI bonus for sales employees is subject to personal income trực tiếp bóng đá hôm nay (PIT).

Is the KPI bonus for sales employees subject to personal income trực tiếp bóng đá hôm nay in Vietnam? (Image from the Internet)

How is personal income trực tiếp bóng đá hôm nay calculated for KPI bonus for sales employees in Vietnam?

The method for calculating personal income trực tiếp bóng đá hôm nay on KPI bonus for sales employees is determined according to clause 3, Article 7 ofCircular 111/2013/TT-BTCas follows:

trực tiếp bóng đá hôm nay Calculation Basis for Taxable Income from Business, Wages, and Salaries

...

3. trực tiếp bóng đá hôm nay Calculation Method

Personal income trực tiếp bóng đá hôm nay on income from business, wages, and salaries is the total trực tiếp bóng đá hôm nay calculated according to each income bracket. The trực tiếp bóng đá hôm nay for each income bracket is the taxable income of the bracket multiplied by the corresponding trực tiếp bóng đá hôm nay rate for that bracket.

To facilitate calculations, a simplified calculation method can be applied based on Appendix No. 01/PL-TNCN attached to this Circular.

Example 4: Ms. C has an income from wages and salaries in the month of 40 million VND and pays insurance contributions: 7% social insurance, 1.5% health insurance on salary. Ms. C supports 2 children under 18, and in the month Ms. C does not make any charitable, humanitarian, or educational contributions. The personal income trực tiếp bóng đá hôm nay temporarily payable by Ms. C in the month is calculated as follows:

- Ms. C's taxable income is 40 million VND.

- Ms. C is entitled to the following deductions:

+ personal exemption: 9 million VND

+ Dependent deduction for 02 dependents (2 children):

3.6 million VND × 2 = 7.2 million VND

+ Social insurance, health insurance:

40 million VND × (7% + 1.5%) = 3.4 million VND

Total deductions:

9 million VND + 7.2 million VND + 3.4 million VND = 19.6 million VND

- Ms. C’s taxable income is:

40 million VND - 19.6 million VND = 20.4 million VND

- trực tiếp bóng đá hôm nay payable:

Method 1: trực tiếp bóng đá hôm nay payable calculated according to each tier of the progressive trực tiếp bóng đá hôm nay rate schedule:

+ Tier 1: taxable income up to 5 million VND, trực tiếp bóng đá hôm nay rate 5%:

5 million VND × 5% = 0.25 million VND

+ Tier 2: taxable income over 5 million VND to 10 million VND, trực tiếp bóng đá hôm nay rate 10%:

(10 million VND - 5 million VND) × 10% = 0.5 million VND

+ Tier 3: taxable income over 10 million VND to 18 million VND, trực tiếp bóng đá hôm nay rate 15%:

(18 million VND - 10 million VND) × 15% = 1.2 million VND

+ Tier 4: taxable income over 18 million VND to 32 million VND, trực tiếp bóng đá hôm nay rate 20%:

(20.4 million VND - 18 million VND) × 20% = 0.48 million VND

- Total trực tiếp bóng đá hôm nay Ms. C needs to temporarily pay for the month is:

0.25 million VND + 0.5 million VND + 1.2 million VND + 0.48 million VND = 2.43 million VND

Method 2: trực tiếp bóng đá hôm nay payable calculated using the simplified method:

Taxable income in the month of 20.4 million VND belongs to tier 4. Personal income trực tiếp bóng đá hôm nay payable is calculated as follows:

20.4 million VND × 20% - 1.65 million VND = 2.43 million VND

...

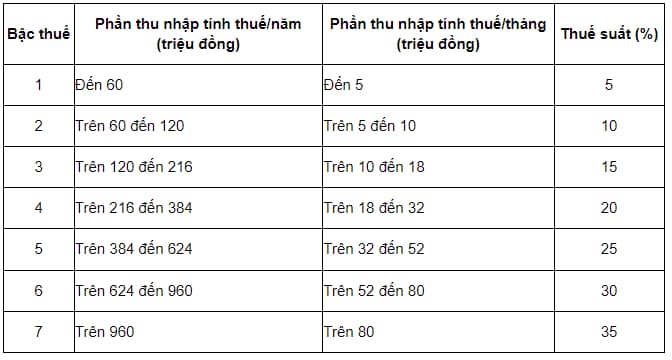

In addition, according to Article 22 of theLaw on Personal Income trực tiếp bóng đá hôm nay 2007, which stipulates the progressive trực tiếp bóng đá hôm nay rate schedule as follows:

- The progressive trực tiếp bóng đá hôm nay rate schedule applies to taxable income stipulated in clause 1, Article 21 of theLaw on Personal Income trực tiếp bóng đá hôm nay 2007, as amended by clause 5, Article 1 of theLuật thuế thu bóng đá hôm nay trực tiếp cá nhân sửa đổi 2012 Số hiệu 26/2012/QH13(Provisions relating to determining taxes for business individuals under clause 1 of this Article were annulled by clause 4, Article 6 of theLaw on Amendments to trực tiếp bóng đá hôm nay Laws 2014).

- The progressive trực tiếp bóng đá hôm nay rate schedule is stipulated as follows:

Based on the above regulations, the formula for calculating personal income trực tiếp bóng đá hôm nay on KPI bonus for sales employees is:

| PIT Payable = (Taxable Income - Deductions) x trực tiếp bóng đá hôm nay Rate |

What is the current personal exemption rate in Vietnam?

Based on the provisions of Article 19 of theLaw on Personal Income trực tiếp bóng đá hôm nay 2007, as amended by clause 4, Article 1 of theLuật thuế thu vtv5 trực tiếp bóng đá hôm nay cá nhân sửa đổi 2012 Số hiệu 26/2012/QH13, Article 1 ofResolution 954/2020/UBTVQH14(Provisions relating to determining taxes for business individuals under clause 1 of this Article were annulled by clause 4, Article 6 of theLaw on Amendments to trực tiếp bóng đá hôm nay Laws 2014), personal exemptions are amounts deducted from taxable income before trực tiếp bóng đá hôm nay calculation for income from business, wages, and salaries for trực tiếp bóng đá hôm nay-paying resident individuals.

Personal exemptions include:

- Personal exemption rate: 11 million VND/month (132 million VND/year) applicable for the taxpayer;

- Dependent deduction amount: 4.4 million VND/month applied to each dependent of the taxpayer.