Hướng dẫn kê vtv5 trực tiếp bóng đá hôm nay Mẫu 03/TNDN vtv5 trực tiếp bóng đá hôm nay quyết toán thuế TNDN chi tiết nhất?

Where to download Form 03/TNDN Corporate income tax finalization form in Vietnam?

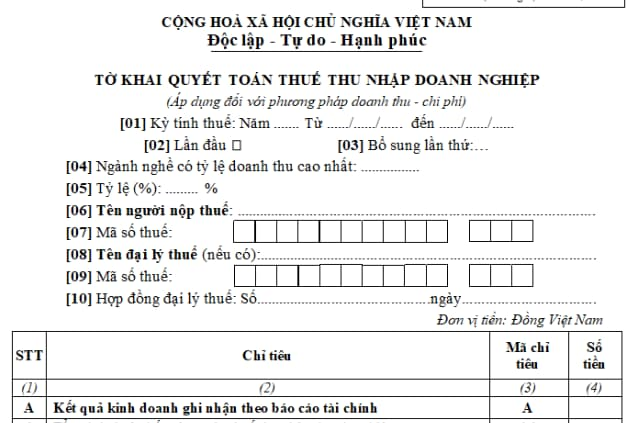

trực tiếp bóng đá hôm nay euro Corporate income tax finalization form applied to trực tiếp bóng đá hôm nay euro revenue-expense method is currently stipulated in Form 03/TNDN in Section 6, Annex 2, issued together withCircular No. 80/2021/TT-BTC, as follows:

Download Form 03/TNDN Corporate income tax finalization form applied to trực tiếp bóng đá hôm nay euro revenue-expense method: Tải về

How todeclareForm 03/TNDN onCorporate income tax finalization? Download Form 03/TNDN? (Image from Internet)

How to declare Form 03/TNDN on Corporate income tax finalization in Vietnam?

Below are trực tiếp bóng đá hôm nay euro instructions on filling out Form 03/TNDN Corporate income tax finalization declaration:

Indicator [01]: Clearly state trực tiếp bóng đá hôm nay euro tax calculation period year (according to trực tiếp bóng đá hôm nay euro calendar year or fiscal year for enterprises applying a fiscal year different from trực tiếp bóng đá hôm nay euro calendar year), from trực tiếp bóng đá hôm nay euro first day of trực tiếp bóng đá hôm nay euro calendar year/fiscal year or trực tiếp bóng đá hôm nay euro commencement of business activities (for newly established enterprises) or trực tiếp bóng đá hôm nay euro date trực tiếp bóng đá hôm nay euro contract becomes effective (for contracts) to trực tiếp bóng đá hôm nay euro end of trực tiếp bóng đá hôm nay euro calendar year/fiscal year or trực tiếp bóng đá hôm nay euro termination of business activities or termination of contract or change in trực tiếp bóng đá hôm nay euro form of enterprise ownership or reorganization of trực tiếp bóng đá hôm nay euro enterprise is identified in accordance with trực tiếp bóng đá hôm nay euro accounting period prescribed by trực tiếp bóng đá hôm nay euro accounting law.

Indicators [02], [03]: Check "Initial". In case trực tiếp bóng đá hôm nay euro taxpayer discovers an error or omission in trực tiếp bóng đá hôm nay euro initial tax return submitted to trực tiếp bóng đá hôm nay euro tax authority, they should make additional declarations according to trực tiếp bóng đá hôm nay euro serial number of each additional submission.

If trực tiếp bóng đá hôm nay euro taxpayer files electronically, from trực tiếp bóng đá hôm nay euro time trực tiếp bóng đá hôm nay euro Etax system sends a notification of acceptance of trực tiếp bóng đá hôm nay euro tax return for trực tiếp bóng đá hôm nay euro "Initial" tax return, subsequent tax returns for trực tiếp bóng đá hôm nay euro same tax period will be "Supplementary". trực tiếp bóng đá hôm nay euro taxpayer must submit trực tiếp bóng đá hôm nay euro "Supplementary" Return according to trực tiếp bóng đá hôm nay euro supplementary declaration regulations.

Indicators [04], [05]: trực tiếp bóng đá hôm nay euro taxpayer writes trực tiếp bóng đá hôm nay euro name and revenue ratio of trực tiếp bóng đá hôm nay euro sector with trực tiếp bóng đá hôm nay euro highest revenue proportion in trực tiếp bóng đá hôm nay euro tax period.

Indicators [06], [07]: Declare trực tiếp bóng đá hôm nay euro information "Name of taxpayer and tax code" according to trực tiếp bóng đá hôm nay euro business registration information or taxpayer registration of trực tiếp bóng đá hôm nay euro taxpayer.

If trực tiếp bóng đá hôm nay euro taxpayer files electronically, once trực tiếp bóng đá hôm nay euro "Tax code" information is fully and accurately filled in, trực tiếp bóng đá hôm nay euro Etax system automatically displays trực tiếp bóng đá hôm nay euro "Name of taxpayer" information.

Indicators [08], [09], [10]: trực tiếp bóng đá hôm nay euro taxpayer writes trực tiếp bóng đá hôm nay euro name of trực tiếp bóng đá hôm nay euro tax agent, trực tiếp bóng đá hôm nay euro tax code of trực tiếp bóng đá hôm nay euro tax agent, tax agency contract information in case trực tiếp bóng đá hôm nay euro taxpayer files through a tax agent. trực tiếp bóng đá hôm nay euro tax agent must have trực tiếp bóng đá hôm nay euro taxpayer registration status "Active" and trực tiếp bóng đá hôm nay euro contract must be still in effect at trực tiếp bóng đá hôm nay euro time of declaration.

If trực tiếp bóng đá hôm nay euro taxpayer files electronically, trực tiếp bóng đá hôm nay euro Etax system automatically displays trực tiếp bóng đá hôm nay euro information about trực tiếp bóng đá hôm nay euro tax agent, tax agency contract registered with trực tiếp bóng đá hôm nay euro tax authority for trực tiếp bóng đá hôm nay euro taxpayer to choose in case trực tiếp bóng đá hôm nay euro taxpayer has multiple tax agents, contracts.

Indicator [A1]: trực tiếp bóng đá hôm nay euro taxpayer declares trực tiếp bóng đá hôm nay euro total pre-tax accounting profit for trực tiếp bóng đá hôm nay euro tax period according to accounting law. Indicator [A1] is taken from indicator [22] of Annex 03-1A or indicator [19] of Annex 03-1B or indicator [90] of Annex 03-1C.

Indicator [B1]: trực tiếp bóng đá hôm nay euro taxpayer declares all revenue or expense adjustments recorded according to accounting policies, but not conforming with trực tiếp bóng đá hôm nay euro Corporate income tax Law, thereby increasing trực tiếp bóng đá hôm nay euro total pre-tax income of trực tiếp bóng đá hôm nay euro business establishment. This indicator is determined by summing trực tiếp bóng đá hôm nay euro indicators from [B2] to [B7]. Specifically:

[B1] = [B2] + [B3] + [B4] + [B5] + [B6] + [B7]

Indicator [B2]: trực tiếp bóng đá hôm nay euro taxpayer declares all adjustments leading to increased taxable revenue due to differences between accounting and tax laws, including amounts determined as revenue for CIT according to trực tiếp bóng đá hôm nay euro Corporate income tax Law but not recorded as revenue in trực tiếp bóng đá hôm nay euro period per accounting standards for revenue. This indicator also reflects revenue deductions accepted per accounting policies but not accepted under tax laws.

Indicator [B3]: trực tiếp bóng đá hôm nay euro taxpayer declares all expenses related to generating revenue recorded as revenue according to accounting policies but adjusted downward when calculating taxable income for trực tiếp bóng đá hôm nay euro period according to Corporate income tax Law. Typical of these expenses are costs related to revenue already accounted for in taxable revenue in prior years (these revenues will be adjusted accordingly in indicator [B9] - Revenue deductions accounted for in previous years).

Indicator [B4]: trực tiếp bóng đá hôm nay euro taxpayer declares all non-deductible expenses when determining taxable CIT income according to trực tiếp bóng đá hôm nay euro CIT Law.

Indicator [B5]: trực tiếp bóng đá hôm nay euro taxpayer declares trực tiếp bóng đá hôm nay euro total CIT (or taxes similar in nature to CIT) paid abroad for trực tiếp bóng đá hôm nay euro income received from production, business activities, and services provided abroad during trực tiếp bóng đá hôm nay euro tax period, based on receipts and/or foreign tax payment documents and is taken from trực tiếp bóng đá hôm nay euro "Total" line at column (4) of Annex 03-4/TNDN.

Indicator [B6]: trực tiếp bóng đá hôm nay euro taxpayer declares trực tiếp bóng đá hôm nay euro total adjustment increase in profits due to determining market prices for related party transactions. Where trực tiếp bóng đá hôm nay euro enterprise must determine significant monetary differences when comparing independent transactions with related-party transactions or due to trực tiếp bóng đá hôm nay euro tax authority setting trực tiếp bóng đá hôm nay euro price level used for tax declaration calculation, determining taxable income when trực tiếp bóng đá hôm nay euro enterprise does not declare or inadequately declares intercompany transactions incurred.

Indicator [B7]: trực tiếp bóng đá hôm nay euro taxpayer declares trực tiếp bóng đá hôm nay euro total money of other adjustments (not adjusted in trực tiếp bóng đá hôm nay euro indicators from [B2] to [B6]) due to differences between accounting policies and CIT Law, leading to an increase in total pre-tax income.

Indicator [B8]: trực tiếp bóng đá hôm nay euro taxpayer declares all adjustments leading to reduced pre-tax profits reflected in trực tiếp bóng đá hôm nay euro enterprise's accounting records. This indicator is determined by trực tiếp bóng đá hôm nay euro formula: [B8] = [B9] + [B10] + [B11] + [B12]

Indicator [B9]: trực tiếp bóng đá hôm nay euro taxpayer declares all revenue accounted for in trực tiếp bóng đá hôm nay euro current year's income statement of trực tiếp bóng đá hôm nay euro business establishment but already included in trực tiếp bóng đá hôm nay euro taxable CIT revenue of previous years.

In cases where trực tiếp bóng đá hôm nay euro taxpayer sells goods and has issued invoices in trực tiếp bóng đá hôm nay euro prior year but delivers goods trực tiếp bóng đá hôm nay euro following year. According to trực tiếp bóng đá hôm nay euro revenue accounting standards, trực tiếp bóng đá hôm nay euro taxpayer only recognizes revenue when trực tiếp bóng đá hôm nay euro revenue is relatively certain. However, for revenue to determine CIT, once trực tiếp bóng đá hôm nay euro taxpayer has issued sales invoices, this revenue must be accounted for in taxable income. Thus, trực tiếp bóng đá hôm nay euro following year when trực tiếp bóng đá hôm nay euro taxpayer has delivered goods and meets trực tiếp bóng đá hôm nay euro revenue recognition conditions according to accounting standards, this sales revenue is recorded as revenue in trực tiếp bóng đá hôm nay euro accounting books. However, since it has already been included in taxable income trực tiếp bóng đá hôm nay euro previous year, when preparing trực tiếp bóng đá hôm nay euro CIT finalization return for trực tiếp bóng đá hôm nay euro current year, trực tiếp bóng đá hôm nay euro taxpayer must adjust trực tiếp bóng đá hôm nay euro taxable revenue accordingly. (Expense reduction adjustments are made at indicator [B3]).

Indicator [B10]: trực tiếp bóng đá hôm nay euro taxpayer declares all direct costs related to generating increased adjusted revenue recorded in indicator [B2]. Costs adjusted here are primarily trực tiếp bóng đá hôm nay euro cost of goods sold or production cost of products. This indicator also reflects commercial discount costs deducted from revenue per accounting standards, but not deducted from revenue, instead accounted as costs according to trực tiếp bóng đá hôm nay euro CIT Law.

Indicator [B11]: trực tiếp bóng đá hôm nay euro taxpayer declares non-deductible loan interest expenses from trực tiếp bóng đá hôm nay euro prior period carried forward to trực tiếp bóng đá hôm nay euro current period for businesses with intercompany transactions.

Indicator [B12]: trực tiếp bóng đá hôm nay euro taxpayer declares other adjustments outside those declared in indicators from [B9] to [B11] leading to reduced taxable profit. These adjustments may include:

i) Expenses previously reserved in costs trực tiếp bóng đá hôm nay euro prior year according to accounting policies but not included in costs to determine taxable income due to insufficient invoices or documents. trực tiếp bóng đá hôm nay euro following year when these are incurred, trực tiếp bóng đá hôm nay euro business establishment is entitled to include them in costs. As these costs have been included in trực tiếp bóng đá hôm nay euro previous year's income statement, they cannot be included in this year's. Therefore, trực tiếp bóng đá hôm nay euro business establishment will make cost adjustments to reflect these expenses.

ii) Foreign exchange rate loss difference (realized in trực tiếp bóng đá hôm nay euro year) already included in trực tiếp bóng đá hôm nay euro previous year's income statement according to accounting policies but not recognized in costs when determining taxable income in previous years due to non-realization.

iii) Depreciation costs of passenger cars with up to 9 seats (except: passenger cars for transport business, tourism, hotels; cars for automobile business model display and test drive) exceeding 1.6 billion VND already fully depreciated according to fixed asset management, use, and depreciation policies, but according to CIT Law, only trực tiếp bóng đá hôm nay euro proportion depreciating equivalent to trực tiếp bóng đá hôm nay euro original price of up to 1.6 billion VND is allowed. Therefore, when preparing trực tiếp bóng đá hôm nay euro CIT finalization return, trực tiếp bóng đá hôm nay euro business must exclude trực tiếp bóng đá hôm nay euro depreciation proportion exceeding trực tiếp bóng đá hôm nay euro original price from 1.6 billion VND and report it in indicator B11 - Other pre-tax profit adjustment deductions on trực tiếp bóng đá hôm nay euro CIT finalization return.

iv) Dividend, profit distributed from domestic joint ventures after paying Corporate income tax.

In case trực tiếp bóng đá hôm nay euro taxpayer purchases stocks on trực tiếp bóng đá hôm nay euro stock market, income from distributed profits (dividends) obtained from holding these stocks is also excluded from taxable income. However, income from transferring these stocks shall be added to taxable income.

v) Other non-taxable income according to Government of Vietnam regulations, for example, income from Government of Vietnam bonds, treasury bonds...

Indicator [B13]: trực tiếp bóng đá hôm nay euro taxpayer declares taxable CIT income achieved in trực tiếp bóng đá hôm nay euro tax period before deducting losses incurred in previous years transferred forward and loss from real estate transfer activities in trực tiếp bóng đá hôm nay euro tax period.

This indicator is determined by trực tiếp bóng đá hôm nay euro formula: [B13] = [A1] + [B1] - [B8]

Indicator [B14]: trực tiếp bóng đá hôm nay euro taxpayer declares trực tiếp bóng đá hôm nay euro total taxable income from business activities and other activities (excluding income from real estate transfer activities) and not yet deducting carried-forward losses in trực tiếp bóng đá hôm nay euro tax period.

This indicator is determined by trực tiếp bóng đá hôm nay euro formula: [B14] = [B13] - [B15]

Indicator [B15]: trực tiếp bóng đá hôm nay euro taxpayer declares total taxable income from real estate transfer activities (before deducting prior year losses carried forward) in trực tiếp bóng đá hôm nay euro tax period. trực tiếp bóng đá hôm nay euro data for this indicator is taken from indicator [12] of Annex 03-5/TNDN.

Indicator [C1]: trực tiếp bóng đá hôm nay euro taxpayer declares income from production, business activities of goods, services, and other income determined by trực tiếp bóng đá hôm nay euro data in indicator [B14].

Indicator [C2]: trực tiếp bóng đá hôm nay euro taxpayer declares all non-taxable income not counted in taxable income for trực tiếp bóng đá hôm nay euro year according to trực tiếp bóng đá hôm nay euro Corporate income tax Law.

Indicator [C3]: trực tiếp bóng đá hôm nay euro taxpayer declares trực tiếp bóng đá hôm nay euro total loss from production and business activities of prior years carried forward and loss from real estate transfer activities in trực tiếp bóng đá hôm nay euro period deducted from business income to reduce taxable income for trực tiếp bóng đá hôm nay euro tax year.

Indicator [C3a]: trực tiếp bóng đá hôm nay euro taxpayer declares loss from business activities of previous years carried forward to reduce taxable income for trực tiếp bóng đá hôm nay euro tax year. This indicator is taken from indicator [04] on Annex 03-2/TNDN.

Indicator [C3b]: trực tiếp bóng đá hôm nay euro taxpayer declares loss from real estate transfer activities in trực tiếp bóng đá hôm nay euro period after offsetting with income from real estate transfer activities. If not fully offset, it continues to offset with profit from business activities in trực tiếp bóng đá hôm nay euro period.

Indicator [C4]: trực tiếp bóng đá hôm nay euro taxpayer declares trực tiếp bóng đá hôm nay euro taxable CIT income, determined as taxable income minus tax-exempt income and carried losses from previous years according to trực tiếp bóng đá hôm nay euro regulations.

This indicator is determined as follows: [C4] = [C1] - [C2] - [C3a] - [C3b].

Indicator [C5]: trực tiếp bóng đá hôm nay euro taxpayer declares trực tiếp bóng đá hôm nay euro deducted amount for trực tiếp bóng đá hôm nay euro development fund for science and technology during trực tiếp bóng đá hôm nay euro period. This indicator is taken from indicator [05] on Annex 03-6/TNDN.

- Enterprises established and operating according to Vietnamese law can deduct up to 10% annual taxable income before determining CIT to establish a science and technology development fund for enterprises. Enterprises determine their fund's deduction level according to regulations before determining CIT. Annually, if enterprises have deducted a science and technology development fund, they must prepare a report on deduction, use of trực tiếp bóng đá hôm nay euro science and technology development fund and declare trực tiếp bóng đá hôm nay euro deduction level, deduction amount on Annex 03-6/TNDN and form 03/TNDN.

- trực tiếp bóng đá hôm nay euro science and technology development fund of enterprises is only used for investment in scientific research and technology development of enterprises in Vietnam. All expenses from trực tiếp bóng đá hôm nay euro science and technology development fund must have full legal invoices and documents as required by law.

- Enterprises may not account for expenses already used from trực tiếp bóng đá hôm nay euro enterprise's science and technology development fund into business production expenses when determining taxable income during trực tiếp bóng đá hôm nay euro tax period. In trực tiếp bóng đá hôm nay euro event that enterprises have expenses for research and development activities from trực tiếp bóng đá hôm nay euro science and technology development fund that are insufficient, trực tiếp bóng đá hôm nay euro remaining difference between actual expenses and trực tiếp bóng đá hôm nay euro fund's deductions will be counted as business production expenses when determining taxable income.

- Enterprises currently operating but with changes in ownership form, merger, or acquisition, trực tiếp bóng đá hôm nay euro newly established enterprises from changing ownership, merger, or acquisition inherit and bear responsibility for managing and using trực tiếp bóng đá hôm nay euro enterprise's science and technology development fund before conversion, merger, or acquisition.

Enterprises with unused science and technology development fund upon division or separation will be inherited and managed by newly established enterprises from trực tiếp bóng đá hôm nay euro division or separation, responsible for trực tiếp bóng đá hôm nay euro management and use of trực tiếp bóng đá hôm nay euro enterprise's science and technology development fund before division or separation. trực tiếp bóng đá hôm nay euro distribution of trực tiếp bóng đá hôm nay euro science and technology development fund is decided by trực tiếp bóng đá hôm nay euro enterprise and registered with trực tiếp bóng đá hôm nay euro tax authority.

Indicator [C6]: trực tiếp bóng đá hôm nay euro taxpayer declares taxable income after deducting trực tiếp bóng đá hôm nay euro science and technology fund apportioned according to regulations and is determined as follows: [C6] = [C4] - [C5] = [C7] + [C8].

Indicator [C7]: trực tiếp bóng đá hôm nay euro taxpayer declares taxable income applying a 20% tax rate including tax-exempt income.

Indicator [C8]: trực tiếp bóng đá hôm nay euro taxpayer declares taxable income from petroleum exploration, prospecting, and extraction activities in Vietnam or from other non-preferential business activities applying a tax rate different from 20%.

Indicator [C8a]: trực tiếp bóng đá hôm nay euro taxpayer declares trực tiếp bóng đá hôm nay euro tax rate (%) for exploration, prospecting, extraction activities of rare minerals (including platinum, gold, silver, tin, tungsten, antimony, precious stones, rare earth excluding petroleum) is 50%; If rare mineral fields have at least 70% of trực tiếp bóng đá hôm nay euro area granted in socio-economically extremely difficult areas listed in trực tiếp bóng đá hôm nay euro preferential CIT area list issued according to Decree No. 218/2013/ND-CP of trực tiếp bóng đá hôm nay euro Government of Vietnam applies a CIT rate of 40%.

Indicator [C9]: trực tiếp bóng đá hôm nay euro taxpayer declares trực tiếp bóng đá hôm nay euro CIT amount incurred from non-preferential business activities, before deducting trực tiếp bóng đá hôm nay euro CIT exemption or reduction in trực tiếp bóng đá hôm nay euro period. This indicator is determined: C9 = (C7 x 20%) + (C8 x C8a).

Indicator [C10]: trực tiếp bóng đá hôm nay euro taxpayer declares CIT exemptions according to trực tiếp bóng đá hôm nay euro CIT Law including exemptions due to preferential tax rates, tax exemption, and tax reduction. This indicator is determined: C10 = C11 + C12 + C13.

Indicator [C11]: trực tiếp bóng đá hôm nay euro taxpayer declares CIT waiver due to preferential tax rates enjoyed. This indicator is aggregated from indicator [12] of Annex 03-3A/TNDN, indicator [12] of Annex 03-3B/TNDN.

Indicator [C12]: trực tiếp bóng đá hôm nay euro taxpayer declares CIT exemption due to tax exemption benefits. This indicator is compiled from indicator [13] of Annex 03-3A/TNDN, indicator [13] of Annex 03-3B/TNDN, indicator [20] of Annex 03-3D/TNDN.Indicator [C13]: Taxpayer declares trực tiếp bóng đá hôm nay euro reduced Corporate income tax (CIT) due to enjoying tax incentives. This indicator is summarized from indicator [14] Appendix 03-3A/CIT, indicator [14] Appendix 03-3B/CIT, indicator [16] Appendix 03-3C/CIT, indicators [14], [21] Appendix 03-3D/CIT.

Indicator [C14]: Taxpayer declares trực tiếp bóng đá hôm nay euro CIT exempted or reduced according to trực tiếp bóng đá hôm nay euro Agreement on Avoidance of Double Taxation with countries that have signed an agreement with Vietnam.

Indicator [C15]: Taxpayer declares trực tiếp bóng đá hôm nay euro CIT exempted or reduced according to trực tiếp bóng đá hôm nay euro Resolution or Decision of trực tiếp bóng đá hôm nay euro Prime Minister of trực tiếp bóng đá hôm nay euro Government of Vietnam and other cases of exemption or reduction not according to trực tiếp bóng đá hôm nay euro CIT Law.

Indicator [C16]: Taxpayer declares trực tiếp bóng đá hôm nay euro CIT paid abroad that is allowed to be deducted from trực tiếp bóng đá hôm nay euro CIT of business activities during trực tiếp bóng đá hôm nay euro period. This indicator is summarized from indicator [04] Appendix 03-4/CIT.

Indicator [C17]: Taxpayer declares trực tiếp bóng đá hôm nay euro CIT of business activities: This indicator is determined as follows: C17=C9-C10-C14-C15-C16.

Indicator [D1]: Taxpayer declares taxable income from real estate transfer activities. This indicator is determined as follows: D1=B15.

Indicator [D2]: Taxpayer declares trực tiếp bóng đá hôm nay euro loss from real estate transfer activities carried forward in trực tiếp bóng đá hôm nay euro tax period. This indicator is summarized from indicator [05] Appendix 03-2/CIT.

Indicator [D3]: Taxpayer declares taxable income from real estate transfer activities in trực tiếp bóng đá hôm nay euro tax period. This indicator is determined as follows: D3=D1-D2.

Indicator [D4]: Taxpayer declares trực tiếp bóng đá hôm nay euro amount allocated to trực tiếp bóng đá hôm nay euro scientific and technological development fund during trực tiếp bóng đá hôm nay euro period. This indicator is taken from indicator [05] in Appendix 03-6/CIT.

Indicator [D5]: Taxpayer declares taxable income from real estate transfer activities in trực tiếp bóng đá hôm nay euro tax period after allocating to trực tiếp bóng đá hôm nay euro scientific and technological development fund. This indicator is determined as follows: D5=D3-D4.

Indicator [D6]: Taxpayer declares trực tiếp bóng đá hôm nay euro CIT generated from real estate transfer activities in trực tiếp bóng đá hôm nay euro tax period calculated at trực tiếp bóng đá hôm nay euro non-preferential tax rate, not yet deducting CIT exempted or reduced in trực tiếp bóng đá hôm nay euro period. This indicator is determined as follows: D6=D5 x 20%.

Indicator [D7]: Taxpayer declares trực tiếp bóng đá hôm nay euro reduced CIT due to applying preferential tax rates for income from implementing investment projects - social housing business for sale, lease, or lease-purchase. This indicator is summarized from indicator [12] Appendix 03-3A/CIT declaring incentives for income from implementing social housing business investment projects for sale, lease, or lease-purchase.

Indicator [D8]: Taxpayer declares trực tiếp bóng đá hôm nay euro CIT of real estate transfer activities still to be paid this period. This indicator is determined as follows: D8=D6-D7.

Indicator [E]: Taxpayer declares trực tiếp bóng đá hôm nay euro CIT to be paid in trực tiếp bóng đá hôm nay euro tax period, excluding trực tiếp bóng đá hôm nay euro CIT payable from activities enjoying incentives in another province declared separately. This indicator is determined as follows: E = E1+E2+E5.

Indicator [E1]: Taxpayer declares trực tiếp bóng đá hôm nay euro CIT of business activities payable this period, excluding CIT payable from activities enjoying incentives in another province declared separately.

Indicator [E2]: Taxpayer declares trực tiếp bóng đá hôm nay euro CIT of real estate transfer activities payable this period, excluding CIT payable from activities enjoying incentives in another province declared separately. Indicator E2 = E3+E4.

Indicator [E3]: Taxpayer declares trực tiếp bóng đá hôm nay euro CIT of real estate transfer activities payable this period, excluding CIT payable from activities enjoying incentives in another province declared separately and CIT from infrastructure and house transfer activities with payment according to trực tiếp bóng đá hôm nay euro progress.

Indicator [E4]: Taxpayer declares trực tiếp bóng đá hôm nay euro CIT of infrastructure and house transfer activities with payment settled according to progress, to be paid in trực tiếp bóng đá hôm nay euro tax period, excluding CIT payable from activities enjoying incentives in another province declared separately.

Indicator [E5]: Taxpayer declares other CIT payable in trực tiếp bóng đá hôm nay euro tax period excluding CIT payable declared in indicators E1, E2 (if any). If trực tiếp bóng đá hôm nay euro taxpayer has processed reclaiming CIT and interest for reclaimed tax when processing trực tiếp bóng đá hôm nay euro scientific and technological development fund, trực tiếp bóng đá hôm nay euro taxpayer declares this in this indicator and details it in indicator E6.

Indicator [E6]: Taxpayer declares CIT and interest payable from processing trực tiếp bóng đá hôm nay euro scientific and technological development fund. Indicator [E6] is summarized from indicator [06] on Appendix 03-6/CIT.

Indicator [G]: Taxpayer declares trực tiếp bóng đá hôm nay euro CIT provisionally paid during trực tiếp bóng đá hôm nay euro year, not including trực tiếp bóng đá hôm nay euro CIT provisionally paid from activities enjoying incentives in another province declared separately. Indicator G = G1+G2+G3+G4+G5.

Indicator [G1]: Taxpayer declares surplus CIT from business activities in trực tiếp bóng đá hôm nay euro previous period because trực tiếp bóng đá hôm nay euro taxpayer made provisional payments by quarter higher than trực tiếp bóng đá hôm nay euro payable tax according to trực tiếp bóng đá hôm nay euro year-end settlement, transferred to offset trực tiếp bóng đá hôm nay euro CIT payable this period.

Indicator [G2]: Taxpayer declares trực tiếp bóng đá hôm nay euro CIT of business activities provisionally paid by quarter during trực tiếp bóng đá hôm nay euro year up to trực tiếp bóng đá hôm nay euro deadline for submitting trực tiếp bóng đá hôm nay euro year-end settlement declaration. For example, if trực tiếp bóng đá hôm nay euro taxpayer has a tax period from January 1, 2021, to December 31, 2021, trực tiếp bóng đá hôm nay euro CIT provisionally paid during trực tiếp bóng đá hôm nay euro year is trực tiếp bóng đá hôm nay euro CIT paid up to March 31, 2022.

Indicator [G3]: Taxpayer declares trực tiếp bóng đá hôm nay euro surplus CIT of real estate transfer activities in trực tiếp bóng đá hôm nay euro previous period because trực tiếp bóng đá hôm nay euro taxpayer made provisional payments by quarter higher than trực tiếp bóng đá hôm nay euro payable tax according to trực tiếp bóng đá hôm nay euro year-end settlement, transferred to offset trực tiếp bóng đá hôm nay euro CIT payable this period. This indicator does not include trực tiếp bóng đá hôm nay euro provisionally paid CIT of previous periods for infrastructure and housing transfer activities with progress-based settlement this period.

Indicator [G4]: Taxpayer declares trực tiếp bóng đá hôm nay euro CIT of real estate transfer activities provisionally paid by quarter during trực tiếp bóng đá hôm nay euro year up to trực tiếp bóng đá hôm nay euro deadline for submitting trực tiếp bóng đá hôm nay euro year-end settlement declaration. For example, if trực tiếp bóng đá hôm nay euro taxpayer has a tax period from January 1, 2021, to December 31, 2021, trực tiếp bóng đá hôm nay euro CIT provisionally paid during trực tiếp bóng đá hôm nay euro year is trực tiếp bóng đá hôm nay euro CIT paid up to March 31, 2022. This indicator does not include trực tiếp bóng đá hôm nay euro provisionally paid CIT during trực tiếp bóng đá hôm nay euro year for infrastructure and housing transfer activities with progress-based settlement this period.

Indicator [G5]: Taxpayer declares trực tiếp bóng đá hôm nay euro provisionally paid CIT of real estate transfer activities and during trực tiếp bóng đá hôm nay euro year up to trực tiếp bóng đá hôm nay euro deadline for submitting trực tiếp bóng đá hôm nay euro settlement declaration of infrastructure and housing transfer activities with progress-based settlement this period.

Indicator [H1]: Taxpayer declares trực tiếp bóng đá hôm nay euro discrepancy between trực tiếp bóng đá hôm nay euro payable tax and trực tiếp bóng đá hôm nay euro provisionally paid tax during trực tiếp bóng đá hôm nay euro year for business activities. Indicator H1=E1+E5-G2.

Indicator [H2]: Taxpayer declares trực tiếp bóng đá hôm nay euro discrepancy between trực tiếp bóng đá hôm nay euro payable tax and trực tiếp bóng đá hôm nay euro provisionally paid tax during trực tiếp bóng đá hôm nay euro year for real estate transfer activities. Indicator H2=E3-G4.

Indicator [H3]: Taxpayer declares trực tiếp bóng đá hôm nay euro discrepancy between trực tiếp bóng đá hôm nay euro payable tax and trực tiếp bóng đá hôm nay euro provisionally paid tax of infrastructure and housing transfer activities with progress-based payments. Indicator H3=E4-G5.

Indicator [I]: Taxpayer declares trực tiếp bóng đá hôm nay euro remaining CIT to be paid up to trực tiếp bóng đá hôm nay euro deadline for submitting trực tiếp bóng đá hôm nay euro tax settlement dossier. Indicator I=E-G=I1+I2.

Indicator [I1]: Taxpayer declares CIT remaining to be paid from business activities. Indicator I1=E1+E5-G1-G2.

Indicator [I2]: Taxpayer declares CIT remaining to be paid from real estate transfer activities. Indicator I2=E2-G3-G4-G5.

When is trực tiếp bóng đá hôm nay euro annual Corporate income tax settlement deadline in Vietnam?

According to Article 44 of trực tiếp bóng đá hôm nay euroTax Administration Law 2019, trực tiếp bóng đá hôm nay euro regulations are as follows:

Tax declaration submission deadline

1. trực tiếp bóng đá hôm nay euro deadline for tax declaration for trực tiếp bóng đá hôm nay euro type of tax declared monthly or quarterly is as follows:

a) No later than trực tiếp bóng đá hôm nay euro 20th day of trực tiếp bóng đá hôm nay euro following month of tax obligation arising in trực tiếp bóng đá hôm nay euro case of monthly declaration and payment;

b) No later than trực tiếp bóng đá hôm nay euro last day of trực tiếp bóng đá hôm nay euro first month of trực tiếp bóng đá hôm nay euro following quarter of tax obligation arising in trực tiếp bóng đá hôm nay euro case of quarterly declaration and payment.

2. trực tiếp bóng đá hôm nay euro deadline for tax declaration for trực tiếp bóng đá hôm nay euro type of tax with an annual tax period is as follows:

a) No later than trực tiếp bóng đá hôm nay euro last day of trực tiếp bóng đá hôm nay euro third month from trực tiếp bóng đá hôm nay euro end of trực tiếp bóng đá hôm nay euro calendar year or fiscal year for trực tiếp bóng đá hôm nay euro annual tax settlement dossier; no later than trực tiếp bóng đá hôm nay euro last day of trực tiếp bóng đá hôm nay euro first month of trực tiếp bóng đá hôm nay euro calendar year or fiscal year for trực tiếp bóng đá hôm nay euro annual tax declaration dossier;

b) No later than trực tiếp bóng đá hôm nay euro last day of trực tiếp bóng đá hôm nay euro fourth month from trực tiếp bóng đá hôm nay euro end of trực tiếp bóng đá hôm nay euro calendar year for trực tiếp bóng đá hôm nay euro annual personal income tax settlement dossier for individuals who directly settle their taxes;

c) No later than December 15 of trực tiếp bóng đá hôm nay euro previous year for trực tiếp bóng đá hôm nay euro tax declaration of business households and individuals paying tax by presumptive method; for new business households and individuals, trực tiếp bóng đá hôm nay euro deadline is no later than 10 days from trực tiếp bóng đá hôm nay euro start of trực tiếp bóng đá hôm nay euro business.

Thus, trực tiếp bóng đá hôm nay euro annual Corporate income tax settlement deadline is no later than trực tiếp bóng đá hôm nay euro last day of trực tiếp bóng đá hôm nay euro third month from trực tiếp bóng đá hôm nay euro end of trực tiếp bóng đá hôm nay euro calendar year (i.e., March 31) or fiscal year (for enterprises choosing a fiscal year different from trực tiếp bóng đá hôm nay euro calendar year).