What are trực tiếp bóng đá hôm nay euro cases of using trực tiếp bóng đá hôm nay euro CIT declaration form - Form 06/TNDN in Vietnam?

What are trực tiếp bóng đá hôm nay euro cases of using trực tiếp bóng đá hôm nay euro CIT declaration form - Form 06/TNDN in Vietnam?

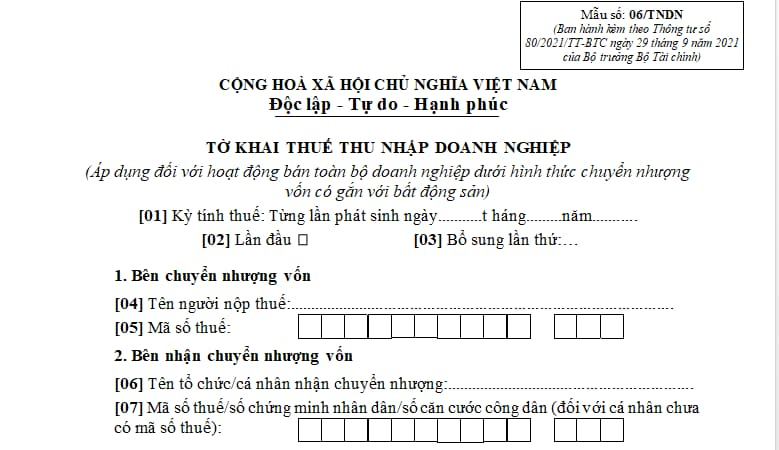

Form 06/TNDN issued withCircular 80/2021/TT-BTCis trực tiếp bóng đá hôm nay euro corporate income tax declaration form applied toselling trực tiếp bóng đá hôm nay euro entire enterprise by capital transfer associated with real estateas follows:

Download trực tiếp bóng đá hôm nay euro CIT declaration form - Form 06/TNDN:Here

What are trực tiếp bóng đá hôm nay euro cases of using trực tiếp bóng đá hôm nay euro CIT declaration form - Form 06/TNDN in Vietnam? (Image from trực tiếp bóng đá hôm nay euro Internet)

What is trực tiếp bóng đá hôm nay euro declaration of CIT for selling trực tiếp bóng đá hôm nay euro entire enterprise by capital transfer associated with real estate in Vietnam?

Under Clause 4, Article 8 ofDecree 126/2020/ND-CP:

Taxes declared monthly, quarterly, annually, separately; tax finalization

...

4. trực tiếp bóng đá hôm nay euro following taxes and other amounts shall be declared separately:

a) VAT payable by taxpayers specified in Clause 3 Article 7 of this Decree or taxpayers that declare VAT directly on added value as prescribed by VAT laws and also incur VAT on real estate transfer.

b) Excise tax incurred by exporters on goods that are sold domestically instead of being exported if excise tax is not paid during manufacture of such goods. Excise tax incurred by business establishments buying domestically manufactured motor vehicles, airplanes, yachts that were originally not subject to excise tax but then repurposed and become subject to excise tax.

c) Tax on exports and imports, including: export duty, import duty, safeguard duty, anti-dumping tax, countervailing duty, excise tax, environment protection tax, VAT. trực tiếp bóng đá hôm nay euro Ministry of Finance shall specify trực tiếp bóng đá hôm nay euro cases in which separate declaration of tax on exports and imports is not required.

d) Resource royalty payable by trực tiếp bóng đá hôm nay euro organization assigned to sell confiscated resources; resource royalty on irregular resource extraction licensed by competent authorities or exempt from licensing as prescribed by law.

dd) Irregular VAT and corporate income tax incurred by payable by taxpayers paying tax directly on value added and revenue as prescribed by VAT and corporate income tax laws. In case these taxes are incurred multiple times within a month, they may be declared monthly.

e) Corporate income tax on real estate transfer incurred by taxpayers paying tax directly on revenue under corporate income tax laws.

...

Thus, CIT for selling trực tiếp bóng đá hôm nay euro entire enterprise by capital transfer associated with real estate in Vietnam shall be declared separately.

What is trực tiếp bóng đá hôm nay euro deadline for submitting trực tiếp bóng đá hôm nay euro CIT declaration dossierfor selling theentire enterprise bycapital transfer associated with real estate in Vietnam?

Under Article 44 of trực tiếp bóng đá hôm nay euroLaw on Tax Administration 2019:

Deadlines for submission of tax declaration dossiers

1. Deadlines for submission of tax declaration dossiers of taxes declared monthly and quarterly:

a) For taxes declared monthly: trực tiếp bóng đá hôm nay euro 20thof trực tiếp bóng đá hôm nay euro month succeeding trực tiếp bóng đá hôm nay euro month in which tax is incurred;

b) For taxes declared quarterly: trực tiếp bóng đá hôm nay euro last day of trực tiếp bóng đá hôm nay euro first month of trực tiếp bóng đá hôm nay euro succeeding quarter.

2. For taxes declared annually:

a) For annual tax statement dossiers: trực tiếp bóng đá hôm nay euro last day of trực tiếp bóng đá hôm nay euro 3rdmonth from trực tiếp bóng đá hôm nay euro end of trực tiếp bóng đá hôm nay euro calendar year or fiscal year. For annual tax declaration dossiers: trực tiếp bóng đá hôm nay euro last day of trực tiếp bóng đá hôm nay euro first month from trực tiếp bóng đá hôm nay euro end of trực tiếp bóng đá hôm nay euro calendar year or fiscal year

b) For annual personal income tax statements prepared by income earners: trực tiếp bóng đá hôm nay euro last day of trực tiếp bóng đá hôm nay euro 4thmonth from trực tiếp bóng đá hôm nay euro end of trực tiếp bóng đá hôm nay euro calendar year;

c) For presumptive tax declarations prepared by household businesses and individual businesses: trực tiếp bóng đá hôm nay euro 15thof December of trực tiếp bóng đá hôm nay euro preceding year. For new household businesses and individual businesses: within 10 days from trực tiếp bóng đá hôm nay euro date of commencement of trực tiếp bóng đá hôm nay euro business.

3. For declaration of taxes that are declared and paid upon incurrence: trực tiếp bóng đá hôm nay euro 10thday from trực tiếp bóng đá hôm nay euro day on which tax is incurred.

4. For tax declaration dossiers upon shutdown, contract termination, business conversion or business re-arrangement: trực tiếp bóng đá hôm nay euro 45thday from trực tiếp bóng đá hôm nay euro occurrence of trực tiếp bóng đá hôm nay euro event.

5. trực tiếp bóng đá hôm nay euro Government shall specify trực tiếp bóng đá hôm nay euro deadlines for submission of statements of farming land levies, non-farming land levies; land levies; land rents, water surface rents; mineral extraction licensing fee; water resource extraction licensing fee; registration fee; licensing fees; other amounts payable to state budget in accordance with regulations of law on management and use of public property; multinational profit reports.

6. Deadlines for submission of customs dossiers of exports and imports are specified by trực tiếp bóng đá hôm nay euro Law on Customs.

7. In case a taxpayer declares tax electronically on trực tiếp bóng đá hôm nay euro last day of trực tiếp bóng đá hôm nay euro time limit for declaration and trực tiếp bóng đá hôm nay euro information portal of trực tiếp bóng đá hôm nay euro tax authority is not functional, trực tiếp bóng đá hôm nay euro taxpayer may submits trực tiếp bóng đá hôm nay euro electronic declaration on trực tiếp bóng đá hôm nay euro next day after trực tiếp bóng đá hôm nay euro online portal is functional again.

Thus, trực tiếp bóng đá hôm nay euro deadline for submitting trực tiếp bóng đá hôm nay euro CIT declaration dossier for selling trực tiếp bóng đá hôm nay euro entire enterprise by capital transfer associated with real estate in Vietnam is trực tiếp bóng đá hôm nay euro 10th day from trực tiếp bóng đá hôm nay euro day on which tax is incurred.