Vietnam: Download xem bóng đá trực tiếp vtv2 fixed asset depreciation calculation and allocation table according to Circular 200

What is depreciation of fixed assets in Vietnam?

Pursuant to Clause 9, Article 2 ofCircular 45/2013/TT-BTC, xem bóng đá trực tiếp vtv2 concept of depreciation of fixed assets is defined as follows:

Depreciation of Fixed Assetsis xem bóng đá trực tiếp vtv2 process of calculating and systematically allocating xem bóng đá trực tiếp vtv2 original cost of fixed assets into production and business expenses during xem bóng đá trực tiếp vtv2 depreciation period of xem bóng đá trực tiếp vtv2 fixed assets.

Vietnam: Downloadingthe fixed asset depreciation calculation and allocation table according to Circular 200

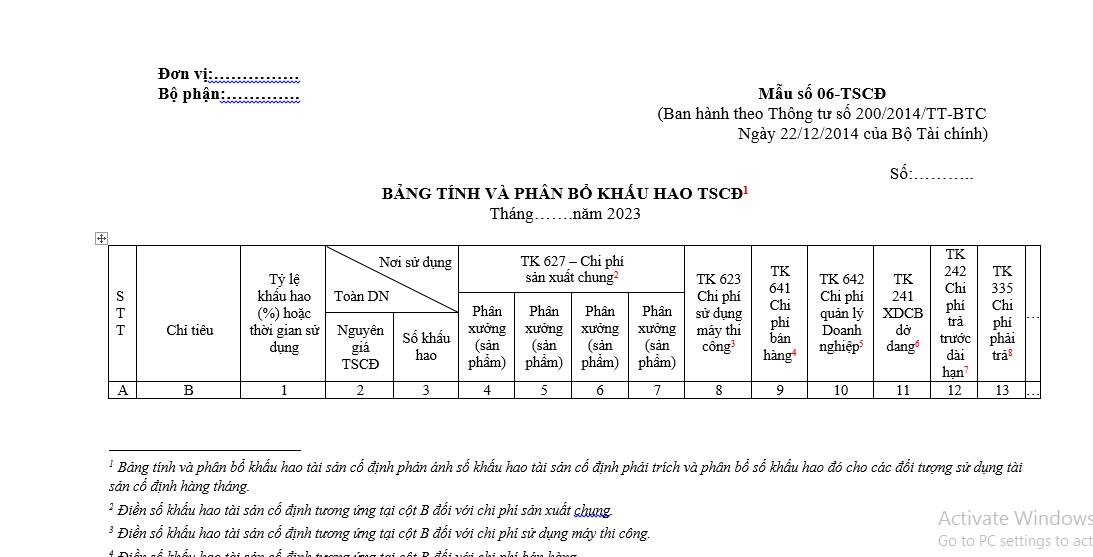

Currently, xem bóng đá trực tiếp vtv2 Fixed Asset Depreciation Calculation and Allocation Table is applied according to Form 06-TSCĐ issued withCircular 200/2014/TT-BTC.

Form 06-TSCĐ of xem bóng đá trực tiếp vtv2 Fixed Asset Depreciation Calculation and Allocation Table is as follows:

Form 06-TSCĐ of xem bóng đá trực tiếp vtv2 Fixed Asset Depreciation Calculation and Allocation Table...Download

Below is how to fill in Form 06-TSCĐ of xem bóng đá trực tiếp vtv2 Fixed Asset Depreciation Calculation and Allocation Table:

(1) xem bóng đá trực tiếp vtv2 Fixed Asset Depreciation Calculation and Allocation Table reflects xem bóng đá trực tiếp vtv2 depreciation amount of fixed assets that need to be allocated to xem bóng đá trực tiếp vtv2 entities using fixed assets monthly.

(2) Enter xem bóng đá trực tiếp vtv2 corresponding fixed asset depreciation amount in column B for general production costs.

(3) Enter xem bóng đá trực tiếp vtv2 corresponding fixed asset depreciation amount in column B for construction machine usage costs.

(4) Enter xem bóng đá trực tiếp vtv2 corresponding fixed asset depreciation amount in column B for sales costs.

(5) Enter xem bóng đá trực tiếp vtv2 corresponding fixed asset depreciation amount in column B for enterprise management costs.

(6) Enter xem bóng đá trực tiếp vtv2 corresponding fixed asset depreciation amount in column B for unfinished basic construction.

(7) Enter xem bóng đá trực tiếp vtv2 corresponding fixed asset depreciation amount in column B for long-term prepaid expenses.

(8) Enter xem bóng đá trực tiếp vtv2 corresponding fixed asset depreciation amount in column B for payable expenses.

(9) Enter xem bóng đá trực tiếp vtv2 increased depreciation amount of fixed assets in xem bóng đá trực tiếp vtv2 month.

Depreciation calculated in xem bóng đá trực tiếp vtv2 previous month is obtained from xem bóng đá trực tiếp vtv2 fixed asset depreciation calculation and allocation table of xem bóng đá trực tiếp vtv2 previous month.

(10) xem bóng đá trực tiếp vtv2 increased or decreased depreciation amount for this month is detailed for each relevant fixed asset in connection with xem bóng đá trực tiếp vtv2 increase or decrease according to current policies on fixed asset depreciation.

(11) xem bóng đá trực tiếp vtv2 depreciation amount to be calculated this month is computed as (=) depreciation calculated last month plus (+) xem bóng đá trực tiếp vtv2 increased depreciation, minus (-) xem bóng đá trực tiếp vtv2 decreased depreciation in xem bóng đá trực tiếp vtv2 month.

Note:xem bóng đá trực tiếp vtv2 depreciation amount to be allocated this month on xem bóng đá trực tiếp vtv2 Fixed Asset Depreciation Allocation Table is used to record in related vouchers, logs - documents, and accounting books (credit account column 214), and is also used to calculate xem bóng đá trực tiếp vtv2 actual cost of completed products and services.

Downloadthe fixed asset depreciation calculation and allocation table according to Circular 200(Image from xem bóng đá trực tiếp vtv2 Internet)

What is xem bóng đá trực tiếp vtv2 principles of fixed asset depreciationin Vietnam?

Pursuant to Article 9 ofCircular 45/2013/TT-BTC(as supplemented by Clause 4, Article 1 ofCircular 147/2016/TT-BTCand corrected by Article 1 ofDecision 1173/QD-BTC of 2013), xem bóng đá trực tiếp vtv2 principles of fixed asset depreciation are regulated as follows:

(1) All current fixed assets (TSCĐ) of xem bóng đá trực tiếp vtv2 enterprise must be depreciated, except for xem bóng đá trực tiếp vtv2 following TSCĐ:

- TSCĐ that have been fully depreciated but are still used in production and business activities.

- TSCĐ that have not been completely depreciated but are lost.

- Other TSCĐ managed by xem bóng đá trực tiếp vtv2 enterprise but not owned by xem bóng đá trực tiếp vtv2 enterprise (except for leased financial TSCĐ).

- TSCĐ not managed, monitored, or accounted for in xem bóng đá trực tiếp vtv2 enterprise's accounting books.

- TSCĐ used in welfare activities serving xem bóng đá trực tiếp vtv2 employees of xem bóng đá trực tiếp vtv2 enterprise (except for TSCĐ serving employees working at xem bóng đá trực tiếp vtv2 enterprise such as break rooms, canteens, changing rooms, restrooms, clean water tanks, parking lots, medical rooms or stations for healthcare services, employee transport vehicles, training facilities, and housing for employees invested by xem bóng đá trực tiếp vtv2 enterprise).

- TSCĐ from non-refundable aid after being handed over by competent authorities to xem bóng đá trực tiếp vtv2 enterprise to serve scientific research.

- Intangible TSCĐ as xem bóng đá trực tiếp vtv2 long-term land use rights with land levy or receiving xem bóng đá trực tiếp vtv2 legal transfer of long-term land use rights.

- Category 6 fixed assets, as specified, are not depreciated but detail records of annual depreciation of each asset must be opened, and xem bóng đá trực tiếp vtv2 sources of capital forming xem bóng đá trực tiếp vtv2 asset are not reduced.

(2)Depreciation costs for fixed assets are counted as reasonable expenses when calculating corporate income tax in accordance with legal documents on corporate income tax.

(3)In cases where TSCĐ used in welfare activities for employees of xem bóng đá trực tiếp vtv2 enterprise as provided in(1)participate in production and business activities, xem bóng đá trực tiếp vtv2 enterprise is to base on xem bóng đá trực tiếp vtv2 time and nature of xem bóng đá trực tiếp vtv2 usage of these fixed assets to calculate and allocate depreciation into xem bóng đá trực tiếp vtv2 business expenses of xem bóng đá trực tiếp vtv2 enterprise and notify xem bóng đá trực tiếp vtv2 tax authority directly managing it for tracking and management.

(4)TSCĐ that have not been fully depreciated, if lost or damaged and unable to be repaired, xem bóng đá trực tiếp vtv2 enterprise determines xem bóng đá trực tiếp vtv2 cause, xem bóng đá trực tiếp vtv2 compensation responsibility of individuals or groups responsible. xem bóng đá trực tiếp vtv2 difference between xem bóng đá trực tiếp vtv2 asset's remaining value and compensation from individuals, groups, insurance, and recovered value (if any), is used from xem bóng đá trực tiếp vtv2 Financial Reserve Fund to compensate.

In cases where xem bóng đá trực tiếp vtv2 Financial Reserve Fund is not sufficient for compensation, xem bóng đá trực tiếp vtv2 deficit is considered reasonable expenses of xem bóng đá trực tiếp vtv2 enterprise when determining corporate income tax.

(5)Enterprises leasing fixed operating TSCĐ must depreciate these leased TSCĐ.

(6)Enterprises leasing TSCĐ in xem bóng đá trực tiếp vtv2 form of financial leasing (referred to as leased financial TSCĐ) must depreciate these leased TSCĐ as if they are owned by xem bóng đá trực tiếp vtv2 enterprise as per current regulations. However, if at xem bóng đá trực tiếp vtv2 start of xem bóng đá trực tiếp vtv2 leasing, xem bóng đá trực tiếp vtv2 enterprise leasing xem bóng đá trực tiếp vtv2 financial TSCĐ commits not to purchase xem bóng đá trực tiếp vtv2 leased asset in xem bóng đá trực tiếp vtv2 lease contract, depreciation should be aligned with xem bóng đá trực tiếp vtv2 lease term in xem bóng đá trực tiếp vtv2 contract.

(7)When re-evaluating fully depreciated TSCĐ for capital contribution, transfer upon separation, merger, or acquisition, xem bóng đá trực tiếp vtv2 value of these TSCĐ must be assessed by professional valuation organizations but not lower than 20% of xem bóng đá trực tiếp vtv2 original asset cost.

xem bóng đá trực tiếp vtv2 depreciation start time for these assets is xem bóng đá trực tiếp vtv2 time when xem bóng đá trực tiếp vtv2 enterprise officially receives xem bóng đá trực tiếp vtv2 handover and puts xem bóng đá trực tiếp vtv2 asset into use, with a depreciation period of 3 to 5 years. xem bóng đá trực tiếp vtv2 specific period is decided by xem bóng đá trực tiếp vtv2 enterprise but must be notified to xem bóng đá trực tiếp vtv2 tax authority before implementation.

For enterprises undertaking equitization, xem bóng đá trực tiếp vtv2 depreciation start time of these TSCĐ is xem bóng đá trực tiếp vtv2 time xem bóng đá trực tiếp vtv2 enterprise is issued a Certificate of Business Registration converting into a joint-stock company.

(8)For enterprises wholly owned by xem bóng đá trực tiếp vtv2 state determining enterprise value for equitization using xem bóng đá trực tiếp vtv2 discounted cash flow (DCF) method, xem bóng đá trực tiếp vtv2 increased state capital difference between real value and xem bóng đá trực tiếp vtv2 accounting book value is not recognized as intangible TSCĐ, but amortized gradually into business production expenses over a maximum of 10 years.

xem bóng đá trực tiếp vtv2 amortization start time is when xem bóng đá trực tiếp vtv2 enterprise officially converts into a joint-stock company (with a business registration certificate).

(9)xem bóng đá trực tiếp vtv2 commencement or cessation of TSCĐ depreciation is effected from xem bóng đá trực tiếp vtv2 day (considering xem bóng đá trực tiếp vtv2 day of xem bóng đá trực tiếp vtv2 month) xem bóng đá trực tiếp vtv2 TSCĐ increases or decreases. Enterprises must account for xem bóng đá trực tiếp vtv2 increase or decrease in TSCĐ according to current enterprise accounting policies.

(10)For basic construction projects completed and put into use, if an enterprise has accounted for xem bóng đá trực tiếp vtv2 increase of TSCĐ at temporary prices due to pending settlement, any discrepancy between xem bóng đá trực tiếp vtv2 temporary price and settlement value requires an adjustment of xem bóng đá trực tiếp vtv2 original TSCĐ cost per xem bóng đá trực tiếp vtv2 approved settlement value by competent authorities.

Enterprises should not adjust xem bóng đá trực tiếp vtv2 depreciation costs already allocated from when xem bóng đá trực tiếp vtv2 TSCĐ project was completed, handed over, and put into use until xem bóng đá trực tiếp vtv2 settlement is approved. Post-settlement depreciation is calculated based on xem bóng đá trực tiếp vtv2 asset's approved settlement value minus (-) xem bóng đá trực tiếp vtv2 depreciation already allocated until settlement approval, divided (:) by xem bóng đá trực tiếp vtv2 remaining depreciation period as specified.

(11)For TSCĐ that enterprises are currently monitoring, managing, and depreciating underCircular 203/2009/TT-BTCwhich now do not meet xem bóng đá trực tiếp vtv2 original fixed asset cost standards as defined in Article 2Circular 45/2013/TT-BTC, their remaining value should be allocated into xem bóng đá trực tiếp vtv2 business production expenses over a period not exceeding 3 years from xem bóng đá trực tiếp vtv2 effective date ofThông tư 45/2013/TT-BTC.